Big Data for Financial Inclusion: Is Boring Better?

By now, most people have heard about the game-changing potential of Big Data, and many are talking about the black-box magic of data-driven predictive analytics. Big Data knows we’re pregnant before we do. Big Data knows where crimes will be committed before they happen. Why shouldn’t Big Data have something to say about how people will use financial services, including whether customers will repay loans?

Alternative data access and analytics can dramatically expand financial access around the world, and over time, the potential gains from effectively leveraging new data will only expand. But for now, much of this talk gets away from the reality of where we are now.

Today, there are very few instances around the world where institutions are making lending decisions based entirely on Big (or alternative) Data analytics. We have not overnight shifted to a world of extending credit solely based on your Facebook friends or Yelp user ratings or a million other data points generated from your daily digital interactions. Sure, people are working on using these data as feeds into existing decision making processes, and initial results are promising, but it’s early.

At the moment, some of the most exciting applications of Big Data analysis are also the most boring. Yes, boring.

Weavers use a hand loom

Weavers use a hand loom

Photo Credit: Chetan Soni

Take for example identity verification. Answering basic question, “Is this person who she says she is?” is a strong determinant of fraud and repayment risk, not to mention a critical first step in complying with “know your customer” regulatory requirements. Traditionally, banks and other financial service providers spend significant time and energy trying to verify customers’ identities, engaging third party firms to make investigations, collecting dozens of documents from customers, and making customers or staff jump through time-consuming hoops on the way to building a customer file and eventually making a yes/no decision.

This is expensive for providers and a big annoyance for customers (in our experience, often 25% or more give up before they even get to a decision). Manual checks, even in developed markets, can often be required for more than 20% of our clients’ applicants. In many emerging markets, it's common for 100% of all applications to require a manual check of some kind (e.g., calling employers, visiting the applicant’s residential address) resulting in slow turnaround times and hundreds of wasted man-hours.

Identity verification may be boring, but it’s definitely important, and a pain point felt across the industry, particularly for traditionally underserved customers like immigrants, students, and other “thin” or no-file individuals.

Solutions like DemystData, which provides data integration software to help financial institutions better access and analyze data (including Big Data), can dramatically simplify this process. Even low-income and underserved customers are leaving significant data trails as they interact in the world, both offline and online, and solutions like Demyst’s can help piece together a range of scattered data points to create single, unified customer profiles yielding high-confidence verifications of identity, employment, income and more. Leveraging alternative data analysis for these verifications can reduce the need for these manual checks and reduce drop-off rates – many of our customers are able to cut these numbers in half or better. For the many underserved customers, passing this first checkpoint can help give access to financial products and services that would otherwise be inaccessible.

As an example, a U.S. lender began using DemystData to streamline the review process and ease the workload of the people doing manual identity reviews. Reviewers can plug in an applicant’s basic data (e.g., business name, applicant name, address, and email) into a dashboard and instantly receive back a basic risk score. This risk model is based not on complicated opaque algorithms but on simple attributes and common sense matching including the estimated age of the business, the distance between addresses found for business and owner, the consistency of the business record across multiple sources, the total amount of information found about the business, the household income of the business owner, whether the applicant could be connected the business through multiple sources, and other similar pieces of information. By combining these attributes and reducing the manual verification requirements, this lender increased acceptance rates by 15%, while achieving an overall lower level of risk.

A second client uses DemystData for real-time validation of phone numbers, physical addresses, and emails. As applicants fill out the online form, DemystData is able to verify the applicant’s information in real-time, allowing the lender to quickly, easily, and cheaply screen for fraud. Again, there’s no magic going on here, just making use of the plethora of available and underutilized data to quickly and accurately check whether each component piece making up an identity is valid, then assessing the likelihood that together they form a real and unique person. This simple process reduced fraud by 12% without adding any friction to the application process.

These two examples demonstrate that Big Data doesn’t have to be black-box, crystal-ball clairvoyance. Instead, taking advantage of cutting-edge technology, analytical tools and data access can make the traditional bottlenecks of lending a little less challenging. For financial inclusion, Big Data is about taking what have been time-, money- and people-intensive processes and making them instant, automated, and cheap. It’s about making it a little easier to say “yes” to customers to whom the financial system has traditionally said “no, no, no.”

Boring? Maybe. Effective? Definitely. Game-changing? Maybe not yet; but this is just the start.

Mark Hookey is the Founder and CEO of DemystData, Paul Breloff is the Managing Director of the Accion Venture Lab.

Also in this Series

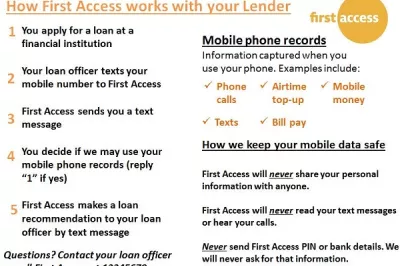

Simple Messages Help Consumers Understand Big Data

After experimenting with SMS messages with Tanzanian microfinance loan applicants, First Access determined that customers can learn a lot about data and their privacy from simple forms of communication.

It's Time to Listen to the Voice of the Consumer

Credit-scoring consumers via advanced analytics on non-traditional data sources has tremendous potential for expanding the boundaries of financial inclusion. Done right, it can deliver cheaper, better financial services to under-served consumers in emerging markets.

Add new comment