Channeling Women’s Potential to Strengthen Last-Mile Agent Networks

Like many women in Papua New Guinea, Kama takes her vegetables to the nearest market every day and returns home with cash in her bilum, a traditional woven purse. For years, she dreamed of saving up enough from her sales to purchase better inputs for the next season and grow produce that fetches higher prices. But with the closest bank branch several hours’ walk away, her only option was to save in cash at home, where her husband’s and male relatives’ financial demands took precedence.

Recently, however, a local bank extended its network of remote agents to a shop she passes on her way home from the market. Kama opened a savings account and now stops by every day to make small deposits. She can confidentially check her balance on her mobile phone and see her savings grow.

Cases similar to Kama’s have been the focus of analysis in CGAP’s global work to understand how to extend the reach and quality of rural cash in/cash out (CICO) agent networks. CICO networks have shown to be one of the critical building blocks of fully digital ecosystems, allowing customers like Kama to convert their cash into e-money and back, enabling them to use available digital financial services (DFS).

In this process of doing this work, we have come to realize that it is critical to apply a gender lens to identify key barriers preventing women — half the population — from utilizing CICO networks.

How can women benefit from CICO networks, and vice versa?

Logic suggests a link between benefits for women as CICO customers and agents and stronger network viability. In theory, a virtuous cycle should exist when CICO access enables women to use financial services that add value to their lives (such as improving their ability to cope with shocks, manage day-to-day needs, and invest in their futures, as Kama hoped to) and their use of these services increases transaction volumes for agents. Since low transaction volumes frequently limit the viability of the agent business model in rural areas, resolving this issue should improve access for people of all genders by strengthening the network itself.

Virtuous cycle between CICO networks and women's financial inclusion

However, the current lack of gender intentionality among most DFS providers means that CICO networks often fall short in serving women. Barriers include gendered social norms that limit what women can do with DFS and how they can interact with male agents, low digital and financial capabilities, lack of products and services designed for women’s business and financial needs, and mobility constraints. Women also face limitations on their time and resources due to their disproportionate share of unpaid household work, such as caring for children and the elderly, cooking, cleaning and other duties.

Gender-intentional CICO networks

“Gender intentional” policies and business practices recognize that people’s needs and experiences with services vary based on their gender, and identify risks and opportunities stemming from this fact. Given the gender imbalances that exist in most countries, services that are not gender-intentional tend to be designed with men in mind as the default user, thereby missing out on women. However, research shows that designing with women in mind doesn’t tend to exclude men. Realizing the virtuous cycle described above requires a gender-intentional approach.

We recommend three basic steps to apply a gender lens to CICO networks at the national or sub-national level:

- Understand women’s financial services needs and their broader contexts. While some may subscribe to the myth that rural women, especially those are not formally employed, don’t use or need financial services, the reality is quite different. In fact, rural women across contexts have varied sources of income, expenses and needs for managing their finances. They are frequent users of informal services, such as borrowing money from friends or pooling savings with groups of neighbors in rotating savings and loans collectives.

Approaches like human-centered design can uncover the ways women currently manage their finances and what challenges they face with the options available. Beyond financial services, it is also important to understand general patterns of women’s lives, including how and where they spend their time, how much control they have over resources and decision-making, what their goals are and what constraints they face to achieving them. These features will vary from place to place and among women in the same place.

- Analyze how CICO networks miss out on women as agents and customers. Increasing the number of active women users and agents will increase the number of agents, as well as their coverage and activity rates. To understand the current gaps and underlying causes, the next step is to overlay gender-based differences in users’ lives, needs and preferences on the stages of the typical user and agent journey. For example, in many cases, the risk of trying something new is higher for women, with greater backlash if something goes awry. To alleviate this, women may need to see more examples of their peers using a service to feel confident that there will be a redress mechanism in case an error results in financial loss.

Examples of questions to consider include: Does the service portray itself as both safe and relevant for women via its marketing, advertisements, and sales process? Similarly, are the requirements to become an agent accessible to women (start-up capital, physical space, means of transportation)? Do gendered social norms inhibit them, such as expectations of who is likely to succeed as an agent or family support for risk-taking and entrepreneurial behavior?

- Develop and test solutions to fill these gaps. The first two steps will identify a number of barriers to which possible solutions can be developed and tested to make CICO networks more inclusive, efficient and reliable in rural areas. For example, Kama’s bank’s understanding of women’s work and family life led them to realize that confidentiality, control and convenience were essential features for women like her. Designing a product with low barriers to entry and services along her usual route enabled the bank to significantly boost its number of women clients.

Testing hypotheses

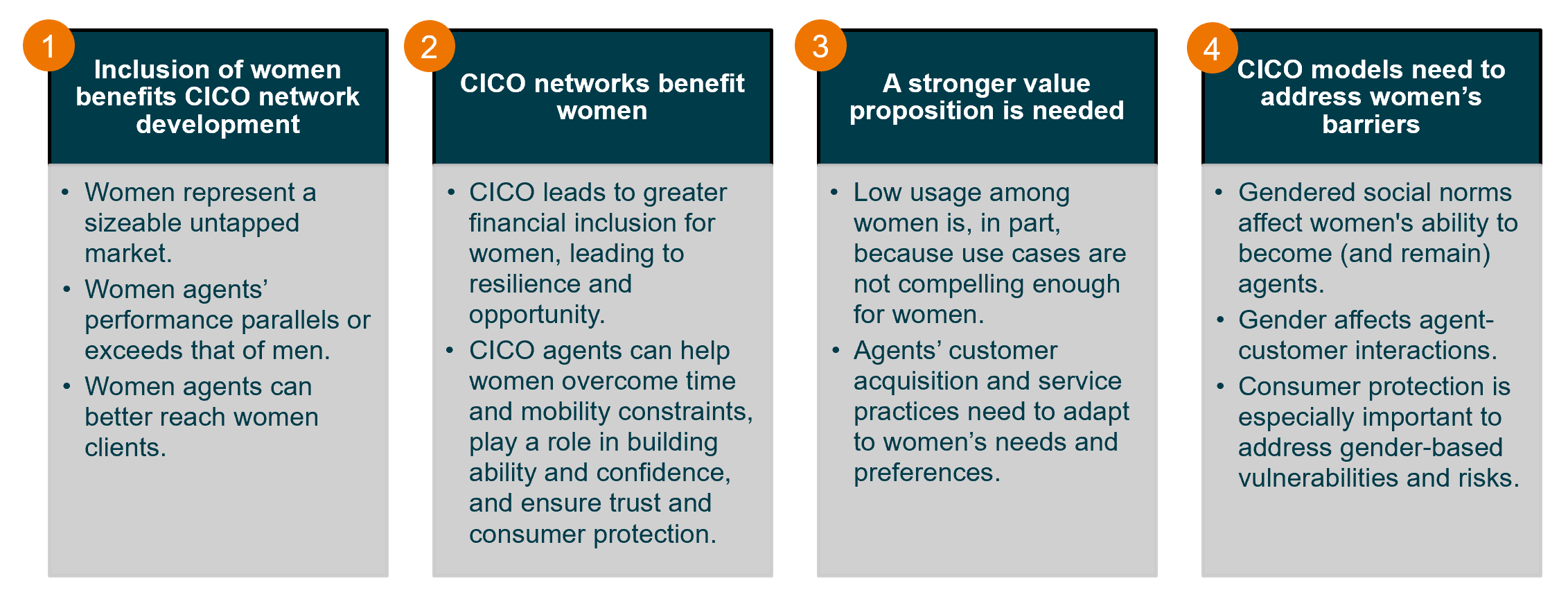

While evidence exists to support some aspects of the virtuous cycle laid out above in discrete contexts, developing practical solutions at the market level will require further validating the assumptions to make a strong case for gender-intentional policy and service delivery. CGAP will test four general hypotheses in six focus countries: Colombia, Cote d’Ivoire, India, Indonesia, Morocco and Pakistan.

Four main hypotheses and underlying assumptions

These hypotheses must be validated and refined through market-level research and by piloting potential solutions for women, which will enable CICO networks to function more effectively for all users and onboard DFS customers in the hardest-to-reach areas.

Over the next two years, as part of a broader effort on agent networks for digital financial inclusion, CGAP will work with partners to test gender-intentional approaches to CICO network development. See this slide deck for a more detailed on how to apply a gender lens to CICO network development.

Resources

This slide deck shows how to apply a gender lens to CICO network development and presents case studies that demonstrate how gender-intentional design works in practice.

")

Add new comment