The digital gig economy holds both promise and pitfalls for low-income workers in Africa, especially women. CGAP’s recent interviews with gig platforms and workers in Kenya suggest that tailored financial services — especially savings products — could help workers better realize the potential of gig work, while minimizing some of the downsides. Importantly, platforms also could benefit from facilitating access to these services. But while platforms across Africa are indeed making credit and insurance increasingly available, savings mechanisms appear under-supplied.

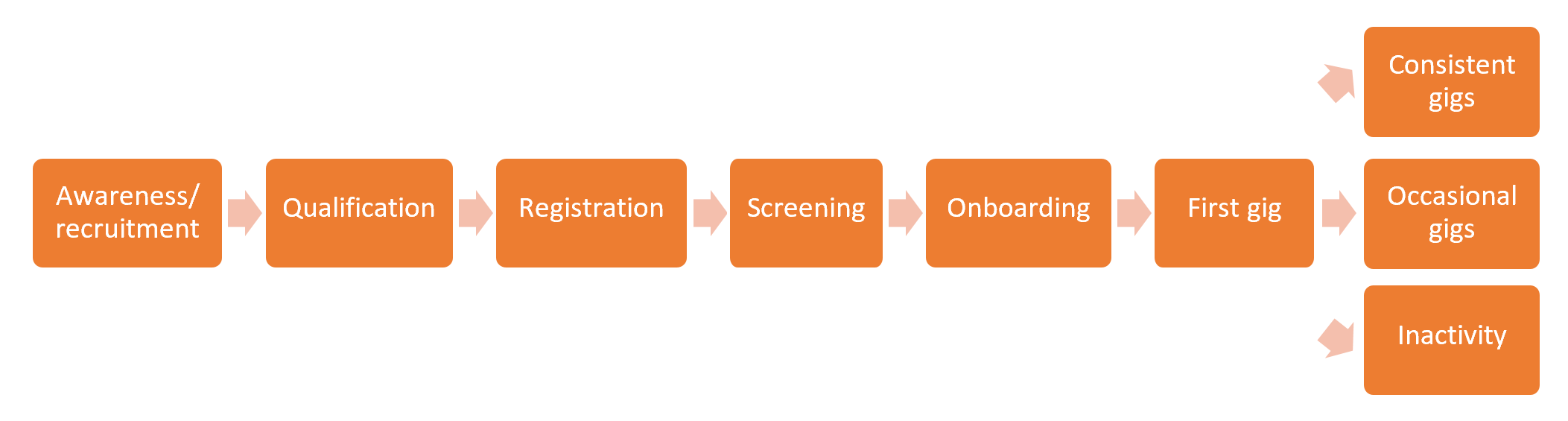

Mapping the gig worker journey

Over the past few months, CGAP has been researching the obstacles and pain points faced by aspiring and current gig workers in Africa, as they enter digital gig work and evolve into consistent, occasional or inactive gig-takers. Our desk research and interviews with eight platforms and 30 workers in Nairobi, Kenya, indicate that although this “gig worker journey” varies by platform and its industry and business model, some pain points are common to workers across platforms. This is significant because it may translate into broadly applicable financial services use cases, increasing the addressable audience and therefore commercial incentives for financial services providers (FSPs) that want to serve platform workers. (Although the segment is growing, these workers still represent a relatively small share of all potential clients in Africa.)

Addressing platform incentives is equally important for sustainable service provision, and the journey map framework helped us pinpoint stages where platforms might find it attractive to make financial services available to workers. The main concerns of most of the platforms we spoke to in Nairobi related to retaining trained workers so that they could seamlessly meet customer demand and control variable costs associated with new workers.

Gig Worker Journey

Our interviews in Kenya have revealed that worker and platform needs intersect in a few key areas relevant to financial services:

Business interruptions due to medical emergencies. Several workers and platforms reported that workers often need to stop work due to illnesses or accidents that affect them or their families. The loss of income can exacerbate the financial consequences of medical emergencies, which push tens of millions of people into extreme poverty every year.

Inability of workers to access equipment on favorable terms. Rental fees charged on everything from ladders to cars can make gig work economically unviable, highlighting the need for affordable financing or effective savings mechanisms to enable workers to acquire required equipment.

Inability of workers to expand their own businesses due to capital constraints. Many platforms we spoke with depend on microbusinesses run by gig workers to fulfill jobs. Larger businesses can more cost-effectively fulfill larger business volumes for the platforms. In many cases, successful gig workers also train new ones, teaching not only technical skills but all-important customer service standards. But such microentrepreneurs often struggle to find expansion capital. They also may face cashflow mismatches, especially in industries such as construction or agriculture, where customer payments come periodically but workers must be paid daily.

Financial services in everyone’s interest

The intersections described above suggest that both workers and platforms may derive value from the following financial services, listed in their order of popularity among the gig worker focus groups we conducted in Nairobi.

A savings mechanism was at the top of workers’ lists by far. They had in mind a financial solution that would lock money safely away from the workers themselves, protecting it from temptation spending and other financial pressures, while still making it available in the case of emergencies. Workers agreed that the ability to set a certain percentage of gig income to be swept automatically into such a savings vehicle would be valuable, as it would considerably ease the frictions to saving. Although they were receptive to doing this through a platform, they did not trust the platform to hold the money itself, preferring instead an account at a reputable financial institution.

Gig workers like Frida Nyawira, a carpenter, often need financing to practice or expand their trade. Photo: CGAPWorking and fixed capital loans were also popular among focus group participants, although second to savings. (In the words of one worker, “Nobody really wants to take a loan – you take a loan because you have to.”) Awareness of the over-indebtedness crisis in Kenya and the consequences of blacklisting in the credit bureaus appeared to be high. Yet workers also expressed a clear need for financing, whether to start, expand or keep a business running. However, workers indicated it would be important for repayments on these loans to be calibrated to their platform income. Stories abounded of loans taken to finance cars for e-hailing that went bad when the rates paid by platforms changed.

Medical insurance offered through platforms also might be taken up by a substantial proportion of workers, especially if benefits and payout processes were made clear and payments were manageable. For example, payments could be made on a daily or even per-gig basis. The rider and driver insurance offered through at least one large e-hailing platform operates in this fashion, and it is valid from the time a driver accepts a trip to the time the trip is officially ended. However, few drivers in our focus groups appeared to be aware this insurance existed or to understand how payout would function in the case of an accident – perhaps because it is paid for by the company. MSC research indicates that responding to the flexibility of gig work using technology and dynamic pricing is also key to serve this market.

The recently updated Cenfri database of gig platforms in Africa found that 52 platforms offer some type of insurance to workers and 25 offer credit – but only three offer a savings facility (in partnership with a licensed FSP) across the eight countries studied. The well-documented economic challenges of offering small-balance savings accounts may be one reason that savings products have not proliferated in this market. But given the equally well-documented impact of savings on the lives of poor people, this may be an area that deserves more attention from donors and financial inclusion actors, who could help facilitate partnerships and support experimentation that could make such services more widely available.

Add new comment