How Sensitive Are Microfinance Clients to Interest Rates?

Many of us have thought for a long time that microcredit clients are not very sensitive to interest rates. But is that actually true? Does the interest rate impact clients’ decision to take the loan, or are most borrowers so eager for reliable credit (or in need of funds right now), that they do not weigh the interest rate of the loan that heavily in their decision to borrow?

A recent CGAP-commissioned study by Innovations for Poverty Action measured borrowers’ sensitivity to interest rates at 132 branches of Mexican MFI Compartamos. A randomized trial offered some potential borrowers a lower interest rate relative to another group of potential borrowers, offering a range of interest rates from 3 to 4.5% a month. The results were interesting:

1. Loan uptake was 22.3% in low-interest rate clusters, versus 15% in high interest-rate clusters. Evidently, interest rates mattered to a substantial numbers of clients.

2. Over an 18-month period, lower interest rate groups took more loans and bigger loans. Take-up rates for the lower interest rate groups were 22.3%, versus 15% amongst the higher interest rate groups. Similarly, average loan size disbursed grew by 21% in the lower interest rate groups post-treatment, resulting in an average loan size that was 4% larger than in the higher interest rate groups post-treatment.

3. Existing clients were particularly influenced by the change in interest rates, with a 17% increase in loans disbursed, versus an 11% increase amongst new clients (defined as their first loan disbursed within the current month). Maybe the existing clients were more sensitive to rate differentials because they had a baseline (the rate on their prior loans) to compare the new rates with?

4. The business case will depend on the individual MFI. In some cases, MFIs might improve profits by lowering their rates, as the revenue gained from doing more lending might exceed the revenue lost due to the lower interest rate. In Compartamos’ case, however, the revenue gains from additional lending did not fully offset the revenue losses from the lower rates. But the balance might tip the other way if other factors are considered—for instance, gains from other services that the new customers eventually buy, or reputational value.

Now that we have some strong evidence that interest rates do matter to many of Compartamos’ borrowers, I think we could benefit from further field trials to answer two additional questions on this topic:

1. Were the new borrowers attracted by the lower interest rates people who would not have borrowed otherwise? In other words, do lower rates produce an increase in aggregate credit use, or do they just move borrowers back and forth among competing MFIs?

2. Beyond the immediate gains and losses from reduced interest rates, can we quantify some of the other elements in the equation? To do so we will need studies of total client profitability that go beyond revenue gains in the first year or two of the client’s relationship with the MFI. Glenn Westley’s recent paper on the business case for small savers looked at marginal rather than average costs, and the profitability of other products eventually sold to the client, and came away with some promising results on long-term client profitability, even if short-term profits weren’t present. Also, does the larger average loan size produced by lower rates bring with it lower operating cost ratios? A $400 loan produces twice the revenue of a $200 loan, but the administrative cost of the two loans might be pretty much the same.

Stay tuned for more work in this area, as CGAP is currently funding two other Innovations for Poverty Action studies of interest rate sensitivity, and we look forward to sharing their results in the future.

Related Blogs

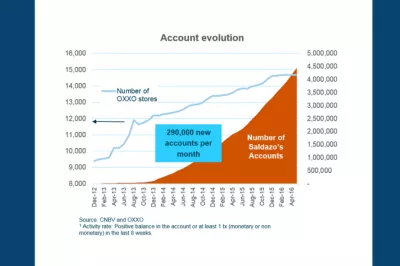

How a Retail Chain Became Mexico’s No. 1 Bank Account Supplier

Saldazo, a Visa debit card product co-branded with Banamex bank, has made Mexico’s largest corner store retail chain – OXXO – the country’s number one transactional account supplier. Here are some key success factors, challenges and insights from this project.

The Replication Limits of M-Pesa in Latin America

Is the challenge of replicating the success of the M-Pesa model in Kenya more about implementation and management or about context and market structure? In Latin America and the Caribbean (LAC), the evidence points to context.

Comments

I have an observation and a

I have an observation and a question:

Observation: Since the lower limit itself is pretty high (3% pm) it is possible that clients feel the pinch already and would not want to borrow at even higher rates (4.5% pm) as much as they would at the lower end. This result may not be as apparent in counties where the lower limit is much smaller, say 2% and upper limit is say 3%.

Question: What is the inflection point when borrowers start showing significant negative reaction to interest rates? In other words, at what rate the uptake starts going down. Is it 0.5% more than lower limit, 1.0 % or 1.5%?

http://devcChandra Babu Naidu

http://devcChandra Babu Naidu ex- Chief Minister who toured the Ranga Reddy district, addressed several micro finance victims and advised them to just pay the principal and not the interest thereupon. He also told them not to make any payments until the government agreed to extend Pavala Vaddi scheme to the Micro Finance. Telling them to tie those who came to their houses for collection of micro debts and throw them in a room, the former chief minister said that his party would then take care of them.

Join the Campaign and ban MFIs. If they want to profit from the blood of the poor, lets give them a taste of their own medicine. Vikram Akula of SKS Microfinance is our mascot

What’s wrong with Micro-finance Institutions? Practically everything as the case of SKS illustrates.

http://devconsultgroup.blogspot.com/2010/10/whats-wrong-with-micro-fina…

Dear All,

Dear All,

I just want to make five points , rather bluntly, about the Andhra Pradesh based my three decade hands on experience of rural financing in India:

a. The justification for regulatory intervention in the MFI Sector in Andhra Pradesh is not sound in as much as it is founded on presumptions and not verified facts. There does not seem to be a whole lot of objective researched evidence to prove the alleged irregularities in the sector or its effects on the poor ?

b. For customer to be protected , the customer needs to be born !In the name of customer protection,let us not kill the only access channel to the financially excluded. After all, people go the MFIs because of the abject failure of the multi-agency strong Indian financial sector.

c. The key thing today is the ACCESS and not the price of the loans to the rural people . In any case, through regulated concessional interest rate of 4 percent Differential Interest Loans Scheme, have the commercial banks been able to reach the people? What has prevented the non-MFI players including the State Government and the various banks and non-banks in Andhra or elsewhere in India from reaching out and enrolling the poor and the excluded? It is simply the NON-VIABILITY of doing business and / or some systemic disability to penetrate the hinterland or both.Before we touch the MFIs , we need to make sure that we do not, however noble and just our intentions maybe,destroy often the only lifeline available to the rural people. The very law which the Government has enacted for protection of the people may , ironically , may block the flow funds.

d.If the MFIs have to work as sustainable and scalable entities and continue to contribute to the financial inclusion as hitherto, the pricing of their products need to be determined by the market forces. Regulatory failures in this sphere in India, at least, dwarf the possible market failures! Nearly six decades of banking policy and regulation has not been able to achieve the reaching of finance to the 80 percent of the population. The magnitude of this failure should make the Governments and the regulators wary of legislating for the MFIs. It may well be the case that MFIs have delivered because they were left alone.

eIn India, at least, it seems the policy makers and policy influencers ,often, want to “dress in borrowed robes” ! Since the South Africa has established a statutory framework for the MFIs, a legislative measure for the MFI regulation is proposed! Since the Bangaldesh Grameen had the lending to the poor as a mission, the Indian MFIs are accused of mission drift when they operate commercially. In my opinion, it is good to regard the MFIs as commercial entities in the financial markets .

All in all, “it is mercy if thou wilt forget !”

Add new comment