Is M-PESA Replacing Cash in Kenya?

The widespread use of credit and debit cards in the developed world and more recently mobile phone payments in the developing world is bringing increasing attention to the idea that, perhaps not far into the future, we may see the first “cashless society.” Kenya, with the cutting edge M-PESA mobile phone payment service, may leapfrog the card-based path to cashless transactions followed in most developed economies to become one of the first countries to become cashless or at least “cash-lite.” Moving toward a cash-lite strategy may have multiple benefits for the poor, including a one, two, three punch improvement in financial management, security and transaction costs.

But how far away is Kenya from the goal of cash-lite? Between July and August 2011, Bankable Frontier Associates (BFA) conducted an intensive field study within an urban and a rural pilot area to study the mode and size of intra-day cash flows at the customer-to-merchant interface and the merchant-to-supplier interface.

Granular data shows that cash is still king

Our field team interviewed and mapped 3,489 businesses in urban areas and 773 in rural areas, equivalent to one merchant for every 13 households in urban and one merchant for every 10 households in rural areas. We then selected 60 retail merchants to collect detailed data over four days, recording the size, frequency and payment medium of transactions.

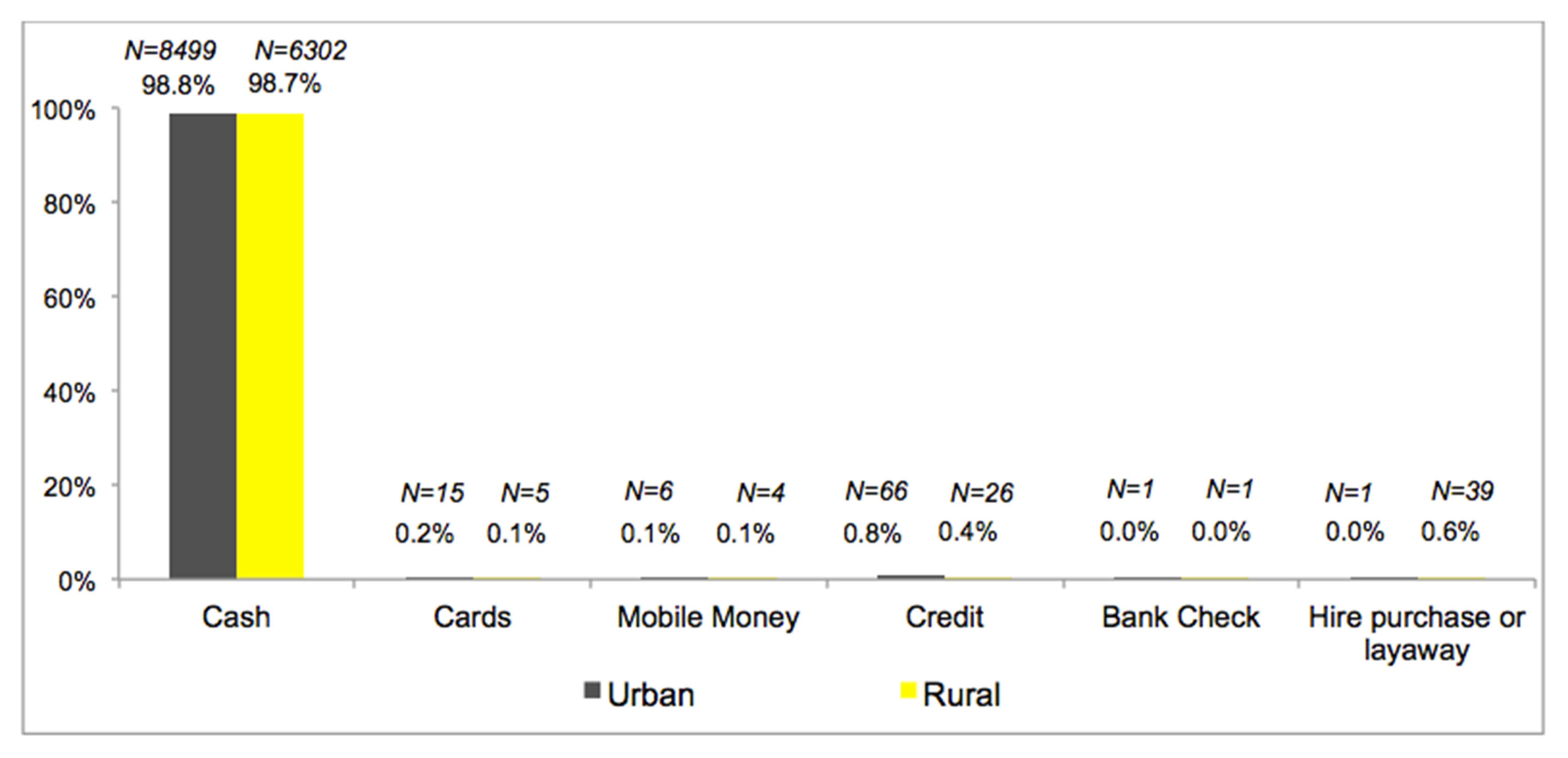

Chart 1: How cash-lite are urban and rural Kenya?

(Share of transactions done with each payment type, with number of transactions observed in parenthesis)

Note that we only recorded transactions that were done in-person, so we did not collect, for example, any repayment of credit done via mobile money.

We discovered that, despite Kenya’s reputation for being a leader in mobile money, cash is still king. As shown in Chart 1, 99% of all retail transactions we captured were done in cash, with most of the remainder done through informal credit arrangements. In contrast, the Payments Council in the UK reports that 59% of consumer transactions were done in cash and accounted for less than one third of transaction values. However, this does not mean that electronic payment is not available from some merchants. Our census data indicated that 18% of retail merchants accept mobile money, while about half will provide short term credit for goods.

Mode of payment varies by transaction size

The 1% of transactions that were done with mobile money accounted for some of the largest payments in the sample. The average transaction size for a mobile money transaction was US$ 75 - in a cash flow environment where two-thirds of transactions were below US$ 3 and the median transaction size was about US$ 1. Fewer than 10% of all transactions in the research were greater than $10.

It seems then that M-PESA has yet to replace cash as a means of exchange for purchases, even in the environments where it has come to dominate the person-to-person remittance space. In our next posting, we’ll unpack what is holding back customers and merchants alike from adopting mobile money as their payment mode of choice for a broader set of their transactions.

Related Blogs

Lessons From 4 Examples on the Leading Edge of Climate-Focused G2P

All G2P programs contribute to climate adaptation to some extent, with examples in India, Ethiopia, Kenya, and the Philippines showing us how specific program design features can support greater climate adaptation for recipients and their households.

Regular Savings from Irregular Income: How Platforms Can Help

CGAP partnered with fintechs and platforms across Sub-Saharan Africa to understand how they are using digital rails to offer savings products to low-income gig workers. Here, we share what we found.

Comments

This looks like a fascinating

This looks like a fascinating study with a good sample size, look forward to the following part(s). It is interesting that we have all had debit cards in the UK for decades but that cash still accounts for more than half of transactions. Mobile money payments are relatively new by comparison, so the insights in the next part of the article on inhibitors to its uptake are keenly awaited.

Perhaps this is also in the next part, but have the authors gained any insights into the overall GDP contribution of mobile money in countries such as Kenya from the work undertaken?

Kevin: thanks very much for

Kevin: thanks very much for your posting and apologies that we didn't get back to you sooner. We didn't in this study attempt to estimate any sort of GDP contribution of mobile money, as we also looked in fine grained detail at two particular areas.

It should be said that the

It should be said that the "first cashless society" was before cash was invented and people used barter...

Hi David

Hi David

Thought you might find this data interesting. Seems we will have to wait for their next posting for an explanation about what is holding back customers and merchants from adopting mobile money!

g

average transaction size for

average transaction size for MM is $75? That sounds pretty high to me. did you ask about what the transactions were for?

thanks, Peter goldstein/InterMedia

Peter: thanks so much for

Peter: thanks so much for your posting and apologies for not responding earlier. The high transaction size is exactly the point - that though we have many an urban legend about paying for small items with M-Pesa, we found that people only used the service for paying with large-scale items, and very infrequently.

Interesting study. But it is

Interesting study. But it is too early to conclude about the speed with which societies like will move to a cashless one. As said in an earlier posting, cash or any order means that is commonly accepted by the people, is necessary to settle balances at all times and even under a barter system.

Most mobile money services

Most mobile money services don't offer an adapted means of using mobile money to pay in stores. I have written papers and given presentations on why this is (e.g. http://www.tagpay.blogspot.fr/2012/05/retail-next-frontier-for-mobile-m…). At the end of the day mobile money can only break the cash-dependence cycle if there is a secure, fast, and user friendly to use your phone to pay a merchant.

Ultimately, for mobile money to be usable in stores a different transaction experience and way of managing merchants is needed. Merchants are fundamentally different from Agents (their business is to sell a good/service and the transaction is just a means to this end). They are also fundamentally different from end-users (a P2P transfer isn't designed to pay merchants).

Today only a handful of mobile money services (for example Celpaid in Ivory Coast and MobiPay in Namibia) successfully offer retail payment as part of their service. It is no suprise that what these services have in common is they use a TagPay platform which includes the Near Sound Data Transfer (NSDT) technology that makes the retail transactions possible.

Hello There,

Hello There,

great content. Would like to read more about mobile money and challenges it posses. From one of the many posts i have read, someone quoted your work. kindly direct me where they are. would like to read through. thanks and regards

Lipa na MPESA is exclusively

Lipa na MPESA is exclusively for paying merchants. Have you done any research in that area? IT might be interesting to read about

Hi, aguardo ansiosamente as

Hi, aguardo ansiosamente as informações sobre as inibições ao uso do sistema, pelos clientes e comerciantes. certamente será uma grande contribuição para todos nós. e Desde já agradeço por compartilhar!

Tks

I agree with Kossi that it

I agree with Kossi that it is too early to make conclusions. I also don't think that Mpesa was meant to replace cash. It is just electronizing money for faster transfers, payments and store of value. Cash rides on a mind set, which has to change first.

FYI, the way Mpesa is used

FYI, the way Mpesa is used today is not the way it was designed to be used. The owners have been smart enought to adapt the product to the way the consuemrs use it. I would not be surprised if M-comerce platforms replace cash payments in the not so distant future.

If Kenyans only used M-PESA

If Kenyans only used M-PESA for large scale items, perhaps there's another factor at work here; specifically, the safety of carrying relatively larger amounts of cash on one's person. It might be revealing to compare rates of the use of "mobile money" to the crime rate against persons, particularly robbery.

Add new comment