Measuring Financial Health: Not as Easy as It Looks

Over the past year, the Center for Financial Services Innovation (CFSI) and the Center for Financial Inclusion (CFI) have explored financial health in emerging markets. We wanted to understand whether the concept of financial health, promoted widely in the United States by CFSI, could be used as a relevant framework to understand consumers. Financial health is defined as coming about when your daily systems help you build resilience and pursue opportunities. Our working hypothesis was that financial health could serve as a method of tracking progress in emerging markets since it is what people strive to attain, and therefore is one of the core aims of financial inclusion.

Our work took us to rural and urban areas in Kenya and India. With the help of the Dalberg Design Impact Group and funding from the Bill & Melinda Gates Foundation, we asked consumers in these markets questions about their financial lives. These questions ranged from how much money they could come up with if they liquidated all of their assets to whether their friends would help them financially in case of an emergency (and about a hundred other questions in between these two ends of the spectrum).

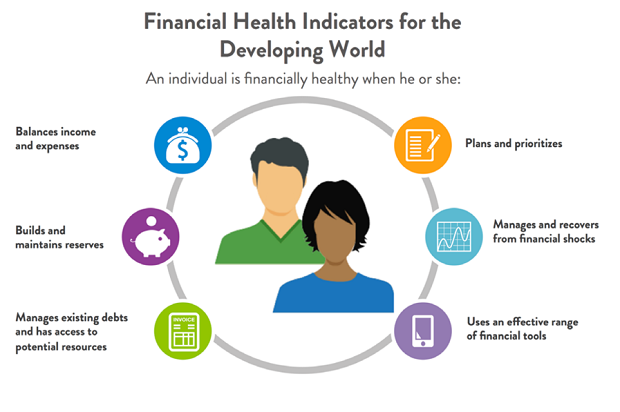

The aim of the research was to identify the key indicators of financial health in a developing world context, similar to the eight key indicators that CFSI had identified for the U.S. market. We found that while financial health as a concept holds in countries like India and Kenya, the indicators to define and measure financial health look somewhat different from those in the United States. The resulting framework can be summed up as follows (and the full report is here).

While a range of stakeholders, including representatives from CGAP, agreed with the overall framework of financial health in developing countries, we discovered three significant challenges in the actual measurement of it.

1. Translating abstract concepts into measurable questions

Understanding people’s financial lives is incredibly complex and not always clear by asking simple, indicative questions. This differs from the situation in the United States, where CFSI undertook consumer-level research on financial health and was effectively able to provide figures behind how consumers spend, save, borrow, and plan.

Whereas most American respondents have bank accounts, tax records and other formal financial transactions that document their financial lives, most interviewees in India and Kenya conduct their financial lives outside the formal financial system. To arrive at the concept of balancing income and expenses, for example, we were forced to ask a question about an individual’s perception of his or her expenses relative to income by providing multiple choice answers such as:

- We often don’t have enough money for food

- We have enough money for basic items such as food, clothes, and school fees, but not enough money to buy expensive good such as a refrigerator and a television

- We can afford to buy certain expensive goods such as a refrigerator and a television

- We can afford to buy whatever we want

However, what we found was that this question may have incorrectly assumed that “basic” items are food, clothes, and school fees, and “expensive” items are TVs and refrigerators. We found that people do not have such a simple hierarchy of needs. An aggressive, risk-taking entrepreneur may give up regular meals for the sake of significant investment in expensive inputs in her business. One woman we talked with, who often did not have enough money for food, said that if she had a cash windfall she would buy a television rather than food so her children could distract themselves from the realities of their life.

2. Ensuring questions are phrased in ways that generate trustworthy and comparable responses

Even when we got the questions “right,” we were not always confident in how our respondents interpreted them. For example, we wanted to understand people’s level of resilience to financial shocks, so we asked, “Has your household witnessed any of the following shocks in the last 12 months?” Then we listed about 10 possible shocks, such as a natural disaster, a job loss or a medical emergency. Our research found that only 30 percent of Indians reported facing shocks over the last 12 months, while in Kenya about 80 percent had faced shocks. Our sample size was far from statistically significant, but from the qualitative interviews that the Dalberg team had done with Indian households prior to the quantitative research, we knew that most households had experienced shocks. Yet they weren’t answering the survey question in a way that seemed accurate to us. Were we defining shocks in a confusing way to them? Did we consider something to be a shock that did not rise to that categorization for these families? We hope the next phase of our work can focus on the difficult, yet important task of designing accurate survey questions to get at some of these nebulous concepts.

3. Understanding the role of contextual factors

As we analyzed the sea of data that we collected from Kenya and India, what rose to the surface, in addition to the direct indicators of financial health, were other factors — more exogenous ones — that had an outsized impact on financial health. These four factors mirror much of CGAP’s work around customer centricity, in particular the insights about how the poor manage their money. We could not justify responsibly measuring financial health without discussing these exogenous or contextual factors, but we also did not want our measurement of financial health to imply that these factors are predictive. For example, we did not want future measures of financial health to imply that moderately low income people with income volatility cannot be financially healthy – though we did conclude that at some very low threshold this may be the case.

Ultimately, we decided not to integrate these factors into the measurement of financial health itself but instead to describe their role in making it easier or harder for people to achieve financial health. Moving forward, these factors will be critical to future surveys in order to better explain variations in financial health on the individual, the community, or even the national level.

As we move forward with this concept, our next steps will be to refine and better test our survey instruments. We are looking forward to continuing to engage with researchers and stakeholders in resolving these challenges of measurement. If you have thoughts either on what we’ve shared here or experiences that could inform this discussion, please leave us a note in the comments below.

Comments

Hi, thanks for this very…

Hi, thanks for this very helpful brief.

Has this work culminated into an index for measuring financial health in a developing country context? Of all the components CFSI/ BMGF/ Dalberg identified, which ones are a stronger indicator and hence, should be assigned a higher 'weight'?

Any inputs on this would be helpful.

Thanks,

Akanksha

Add new comment