More on Why OTC Makes Sense for Kenya

Cash-lite and cashless are current buzzwords in financial inclusion circles. They have become the goal of many business and public policy initiatives especially in the mobile ecosystem. However, usage data puts into question whether these goals really respond to the needs of people at the base of the income pyramid. The first of this two-part article explained that the majority of M-Pesa transactions are one loop, meaning that there is only one electronic transaction before money is cashed out. This article discusses why these customers might be better served by over-the-counter cash transactions rather than e-wallets.

Mobile financial services are so popular because they keep costs low while being more accessible than competing services that rely on physical locations and equipment (such as bank branches, remittance companies or ATMs). M-Pesa’s popularity has little to do with the ability of consumers to open accounts, and more to do with mobile technology enabling agents to make transactions in real-time with minimal hardware and connectivity requirements.

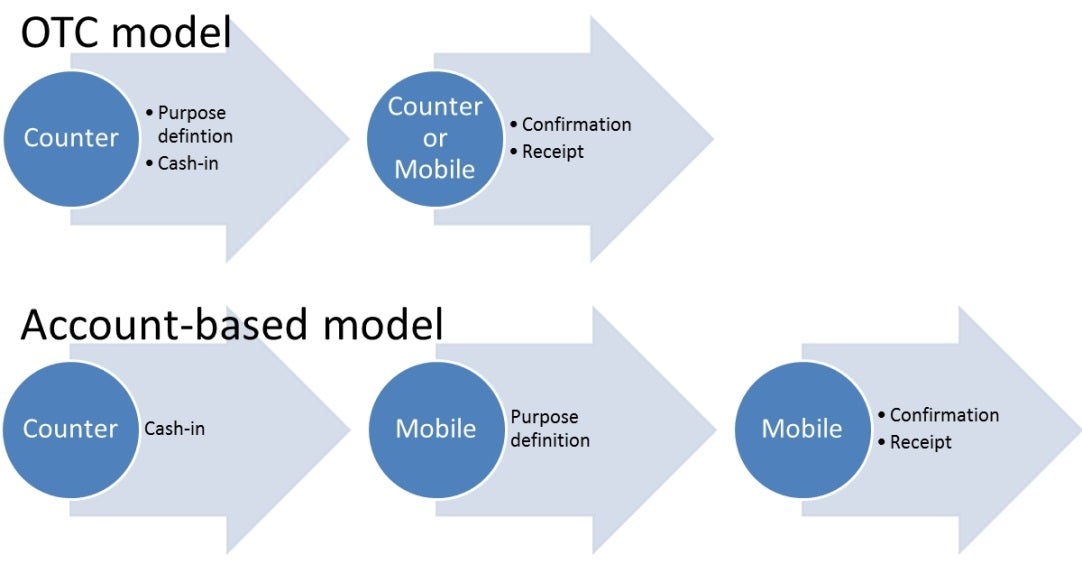

As presented in Part 1 of this article, about two-thirds of the total funds deposited in M-Pesa’s e-wallets are single loop, meaning that there is only one electronic transaction before money is cashed out. This suggests that most customers have a defined purpose for their money at the moment of cash-in.

The fact that most “mobile” transactions require users to visit an agent removes mobile money’s advantage over other cash transfer competitors. If you’re only going to use money once – rather than maintain a running balance and conduct multiple transactions – the e-wallet only adds additional steps to every transaction, making it more inconvenient and even superfluous.

In a recent article, Daniel Radcliffe from the Gates Foundation questioned why Pakistan's mobile money customers aren't opening accounts. The article points out that some users simply believe they do not need one. Being “financially included” is generally equated with having a formal bank account. Even though this assertion is largely unchallenged, it may be misleading. E-wallets thrive not because customers have accounts, but in spite of them. The true innovation of e-wallets is not the electronic account itself, but instead the supporting agent network that increasingly gets bigger and more geographically diverse.

Although the analysis on M-Pesa’s usage data is limited, the broader argument, that people prefer cash to e-wallets, seems applicable to Kenya, and even more so for many other not-so-successful cases. In summary:

- OTC transactional models are suitable for some market segments and enable transactions to reach a critical mass. This does not mean that there is a conflict between OTC and e-wallet models. Instead, these models complement each other - allowing users to choose is always a good idea.

- OTC transactions are a good option in markets where regulatory issues may inhibit the development of mobile banking. Without major reforms, OTC models can deliver quality services and, in many cases, better user experiences (or than mobile services for large segments of underserved populations.

- Widely disbursed agent networks are the standard innovation for both OTC and e-money models.

- E-money models will inevitably gain ground in the longer term, as they have greater potential for innovative services. However, they are not the best option at the outset.

There are many complex reasons why people choose not to use mobile financial services. An imperfect answer to this myriad of issues is to build on preexisting user behavior through efficient OTC transactions. Cashless goals are too focused on designing products that make people want to switch to e-money solutions while, even in Kenya after six years of operations of M-Pesa, people still prefer cash. Focusing on large-scale social change is laudable, but in the meantime it seems practical to design programs based on actual customer needs and to prepare for sweeping change if and when it comes.

----The author is an independent consultant who focuses on business model innovation in the mobile environment.

Also in this Series

Mobile Wallets: Is a Transition Underway in Bangladesh?

E-wallet use is becoming more common in Bangladesh. However, OTC transactions are still very popular and will likely remain so until the process of opening an e-wallet account and using it regularly become easier for and more attractive to the poor.

The “EasyPaisa” Journey from OTC to Wallets in Pakistan

While the founders of EasyPaisa guessed that they would reach a reasonable volume of customers through OTC services, they did not guess that OTC remittances would be the dominant activity by far for EasyPaisa's customers.

Comments

It seems to me that the

It seems to me that the single transaction cash-in/cash-out transactions reflect the large role of remittances in M Pesa. The funds are sent to a group of people where Points of Service are not available, and the economy is basically cash. Even keeping the remittance on the phone and using it to make purchases in a market would be complex.

OTC transaction are most

OTC transaction are most popular among the customers who don't have accounts, irregular users and who feel risk/uncomfortable to make transaction by themselves. Most MFS customers fall in this category. But, all fraud cases related with misuse of MFS are conducted through OTC. that's we are observing in Bangladesh and probably same situation in other market. Criminals have invented new techniques after the emergence of MFS and it is harder to detect those criminals and prececute them. we need to develop transaction model through technological solution to serve the purposes of those segment of OTC customers. we also need to develop supervisory models for MFS.

Add new comment