Some Insights into Over-indebtedness in India

Microfinance Institutions in Andhra Pradesh and elsewhere in India are keen to avoid over-indebtedness or place clients in distress. A joint effort by EDA Rural Systems and CGAP investigated the mass defaults of 2009 in Karnataka. The study draws from a representative survey of 900 customers in two mass defaults towns, Kolar and Ramanagaram and from two nearby comparable comparison towns in Karnataka that did not witness mass defaults (Nanjangud and Davanagere). Both defaulters and non-defaulters were interviewed.

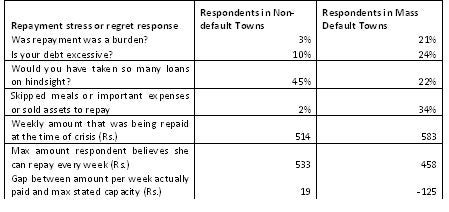

Repayment distress

Since it is difficult to define over-indebtedness, we focused on repayment stress and regret amongst customers about having taken on so many loans on hindsight. The table below shows that many borrowers had taken on more debt than they think they should have, found repayment a burden, wouldn’t have taken on so much debt on hindsight and show symptoms of distress such as skipping meals or important expenses or selling assets to repay.

What explains repayment distress?

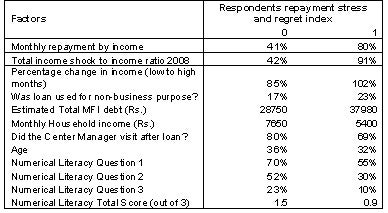

For each respondent, we created an index which is set to “1” if the respondent reported both repayment burden and regret over having taken so much debt on hindsight and zero otherwise. The table below lists factors correlated to this index. In terms of borrower characteristics, lower income (in turn correlated to income variation over the year and income shocks), higher debt, and lower numerical literacy are the main factors. We further find that a customer is more likely to have an index value of one if the Center Manager had not conducted loan utilization checks after disbursement or if she was using the loan for non-business purposes. This suggests that for some customers, using the loan for non-income generating purposes, which may be in part due to fewer loan utilization checks, increases the difficulty to repay.

Financial capability

Customers were asked three questions to gauge numerical literacy. a) You want to buy baskets worth Rs. 47. If you pay the shopkeeper with a 100 Rupee note, how much change will you get? b) Suppose you have weekly instalments of Rs.100 and Rs.200 on two loans respectively. What is your total monthly loan repayment amount? c) Suppose you have 3 loans with weekly repayments of Rs.100, 100 and 200 each. Your monthly income is Rs.5000 and your monthly expenditure is Rs.3300. Suppose you are offered a new loan with weekly repayment of Rs.50, can you take it and still be able to repay without decreasing your expenses?

It is surprising that large numbers of customers were not able to answer question 1 correctly. We see that the percentage of correct responses is lower among those whose index value is one. We further find that even controlling for other factors such as debt, income, religion, and education and other characteristics, those not being able to answer these questions correctly are more likely to have an index value of 1.

This suggests that while MFIs certainly need to have good credit appraisal and monitoring processes, we cannot always assume that the client can gauge the right amount of debt to take.

Has repayment distress made people worse off?

It is interesting that despite large incidences of repayment stress, only 2% of the clients in the mass default towns reported that their economic lives had become worse after taking MFI loans. Close to 89% said that their household condition had improved because of increased income generation from business and due to lower interest rates of MFI loans compared to outside options, while 9% reported no change. While we should not draw strong conclusions from these self-reported responses, it provides a perspective in the discussion on how much is too much debt for borrowers.

What can MFIs do?

We find that those who report no repayment stress or regret have an average monthly loan repayment to household income ratio of close to 40%. This is consistent across the five questions. While there is a large variance in the values of this ratio around the mean, the average of 40% may be a useful guiding figure in the Indian context.

Augmenting the loan application form to ask a couple of simple numeracy questions will help identify some high risk clients at low cost. Asking the customer a simple verifiable question such as how much can she repay every week given her stated current monthly income and expenses is easily done. If she gets it wrong, she could offered a smaller loan and monitored more carefully. This further implicitly places more responsibility on the customer to borrow responsibly.

Also in this Series

Over-Indebtedness in Microfinance – Who Should Bear the Risk?

While microfinance products and lending methodologies vary significantly on the ground, two main features of microfinance have made this enormous expansion of access to finance possible: microlending has become scalable due to cost efficient operating models and due to risk management methodologies that ensured high repayment rates.

We Need to Keep Learning about Overindebtedness

We need to look more carefully at the interactions between microfinance institutions and their clients, examining how MFI practices play out in lives of clients on an everyday basis. Stuart posed two specific hypotheses: if a lender needs clients to borrow continually, it incentivizes overselling and overindebtedness, and that insistence on immediate, in-full repayment drives some clients to begin bicycling loans.

Comments

Dear Karuna

Dear Karuna

An interesting post with fresh data focusing more on quality dimesion for the subject. However I wish to share a few moot points.

While discussing on the clients’ responsibility, the knowledge on numeracy has been taken as the main factor for judging their financial capability and repayment capability (based on the house hold budget). Although it is necessary for the said purpose, the other important factors which influence contextually more on the repayment and over indebtedness are cited below for which both MFI s and the poor customers have the role to play for execution of responsible lending and borrowing respectively

1. Analysis on credit absorption capacity of the given area/region

2. Formulation of potential linked Micro credit plan for the MFI/SHG

3. Integration of micro credit products with micro insurance and micro savings

4. Integrating repayment mode with the agencies of marketing of the proceeds

5. Integration of income generation period with the repayment schedule

The basic principle in Micro financing is that mere micro credit irrespective of the size of the loan will not deliver the desired good unless it is integrated with other support services . Other wise over indebtedness problem in terms of repayment stress for the clients and recovery stress for the lender continues to prevail.

Rengarajan

Add new comment