Understanding our Smallholder Clients, Serving them Better

Rebecca Muronji is a smallholder farmer working and living in Kenya’s Teso district. She has found a way to supplement her modest farm income with another source of revenue: using her Sun King Pro solar lamp, obtained from One Acre Fund on credit, to charge cell phones for neighbors. Rebecca used to only charge her and her husband’s phones with her Sun King Pro until neighbors started requesting that she charge their phones as well.

Soon, Rebecca’s neighbors were competing against each other, seeing who could arrive at her house earliest to charge their phones. Some even started offering small amounts of money for her to prioritize their phones over others. Eventually, it occurred to Rebecca that charging a set fee, on a first-come-first-serve basis, was the only way to keep the phone charging fair.

This is an example of the complex financial lives of some smallholder farmers. There is amazing ingenuity – and amazing diversity – in how people living in poverty are improving their lives. As we all know, however, much more needs to be done for many more people.

That is why strategic decision-making, certainly when it comes to the funding of programs to reduce poverty, has to be based on data and facts. Any sound and verifiable contribution to our sum knowledge of information about those at the bottom of the pyramid is welcome. For us, this is critical information as we plan ahead and determine our funding priorities. We’re already a major funder of initiatives to drive financial inclusion in Africa. Increasingly, we are investing in the agriculture rural development space. But we, like many others, seek more information about the people we are called upon to serve as we try to answer the question: is our funding achieving the goals we set for our Foundation: to create opportunity for all to learn and prosper.

We know that Africa remains a continent where the majority of people, and a large majority of disadvantaged people, live in rural areas and rely on subsistence agriculture for their livelihoods. Agriculture currently provides a livelihood for more than 70% of sub-Saharan African households.

We also know that most smallholder farmers could produce more with the right inputs, the right finance skills, and the right access to markets. Smallholder farmers are amongst the most financially excluded of all client segments. Understanding their particular needs is an important step in helping financial service providers to develop appropriate and effective products that serve their unique needs. These needs probably include, for example, savings products to help them manage cash flow and build assets, insurance products to mitigate risk, and flexible credit products to help them manage their farms and off farm activities.

The importance of keeping client needs at the center of product design and delivery is a key component of The MasterCard Foundation’s work to broaden and deepen access to financial services. To increase understanding of clients and their experiences with financial services, we introduced a “Client Journey” framework at the 2014 Symposium on Financial Inclusion. This allowed us to focus on understanding what prompts poor people to embrace new products and services, how institutions engage with clients and understand how they manage their money, and which activities and product designs prompt clients to use financial services effectively, share their experiences with others to build trust, and then regularly use these products and services.

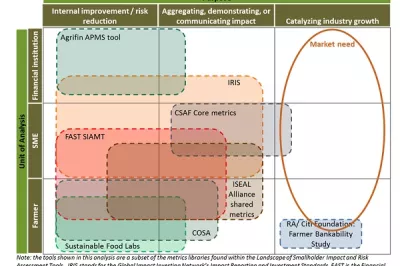

This “client journey” framework resonates strongly with many practitioners. Effectively designing and delivering client-focused products, however, requires a full understanding of the financial needs and complex financial lives of specific client segments. Currently, this is what is most lacking in the case of smallholder farmers.

The CGAP smallholder financial diaries will provide much needed information on how smallholder households earn, save, and spend their money. This knowledge is critical for understanding this segment’s needs so that financial services can be developed to best serve it. CGAP’s planned national surveys in Tanzania and Mozambique will complement the diaries and help to round out the picture in terms of both the demand for and the supply of appropriate products. Together, these two important pieces of research will help to fill the knowledge gap – and help funders such as us to make better strategic decisions.

At The MasterCard Foundation, we are expanding our partnerships that address the financial services needs of smallholder farmers in Africa. We know that people making up this segment are underserved and that access to finance is a one of several challenges that they face in growing their farming activities.

Financial service participants at our Symposium in July said that they are very interested in learning how to develop products and services with client needs more in mind; this was one of the primary reasons why they were attending the Symposium. Understanding the lives of clients, and their particular needs, is a first step in the client-centric development of products and services. And that itself is a critical step in enabling the poor to seize opportunity and develop their own pathways out of poverty.

Moving forward, we hope that Rebecca Muronji and other often-neglected smallholder farmers in Africa will move front and center on the radar screens of financial service providers, and that both groups will appreciate the real benefits of what the other has to offer.

Also in this Series

Filling the Smallholder Household Data Gap: A New Learning Agenda

There is a significant data gap when it comes to smallholders' demand for financial services. Filling this gap is going to require new efforts and a shared learning agenda.

Learning from Smallholder Supply Chains in Côte d’Ivoire

IFC and Ecom, a global commodity trading company, interviewed more than 2,000 cocoa farmers in Côte d’Ivoire about their income levels, food security, and other qualitative aspects of their farming lives. The results highlight some key challenges facing smallholder farmers.

Add new comment