What’s Financial Health Got to Do with It?

Over the past few years, concepts related to financial health and well-being have become more prominent within financial inclusion circles. But what is the relationship between financial inclusion and financial health? CGAP has taken a deeper look into the origin and purpose of financial health and well-being concepts and tried to assess their relevance for advancing financial inclusion in emerging economies. While we see value in these concepts for a few reasons, we also think it’s important to interrogate their universal applicability and seemingly obvious link to financial inclusion.

The many meanings of financial health

Concepts related to financial health go back many years, but financial health really made an entrance in 2015 when CFSI published its first Consumer Financial Health Study and the U.S. Consumer Financial Protection Bureau began publishing on the related concept of financial well-being. Since then, the Bill & Melinda Gates Foundation, CFI, CFSI and Dalberg have published a report that measures financial health in two emerging markets, India and Kenya; the Central Bank of Brazil has conducted surveys; and Gallup, funded by MetLife Foundation, has surveyed people in 10 countries on financial control and security. Meanwhile, academics have made significant progress researching the determinants of financial health and improving how it’s measured.

Although there’s not a universal definition of financial health, the examples listed above share some commonalities. For example, they are usually normative — meaning they are built around a set of “optimal” behaviors or outcomes against which individuals are measured. Most definitions include the following elements: day-to-day financial management, resilience, the ability to take advantage of opportunities or pursue financial goals and feeling in control of and secure in one’s financial future.

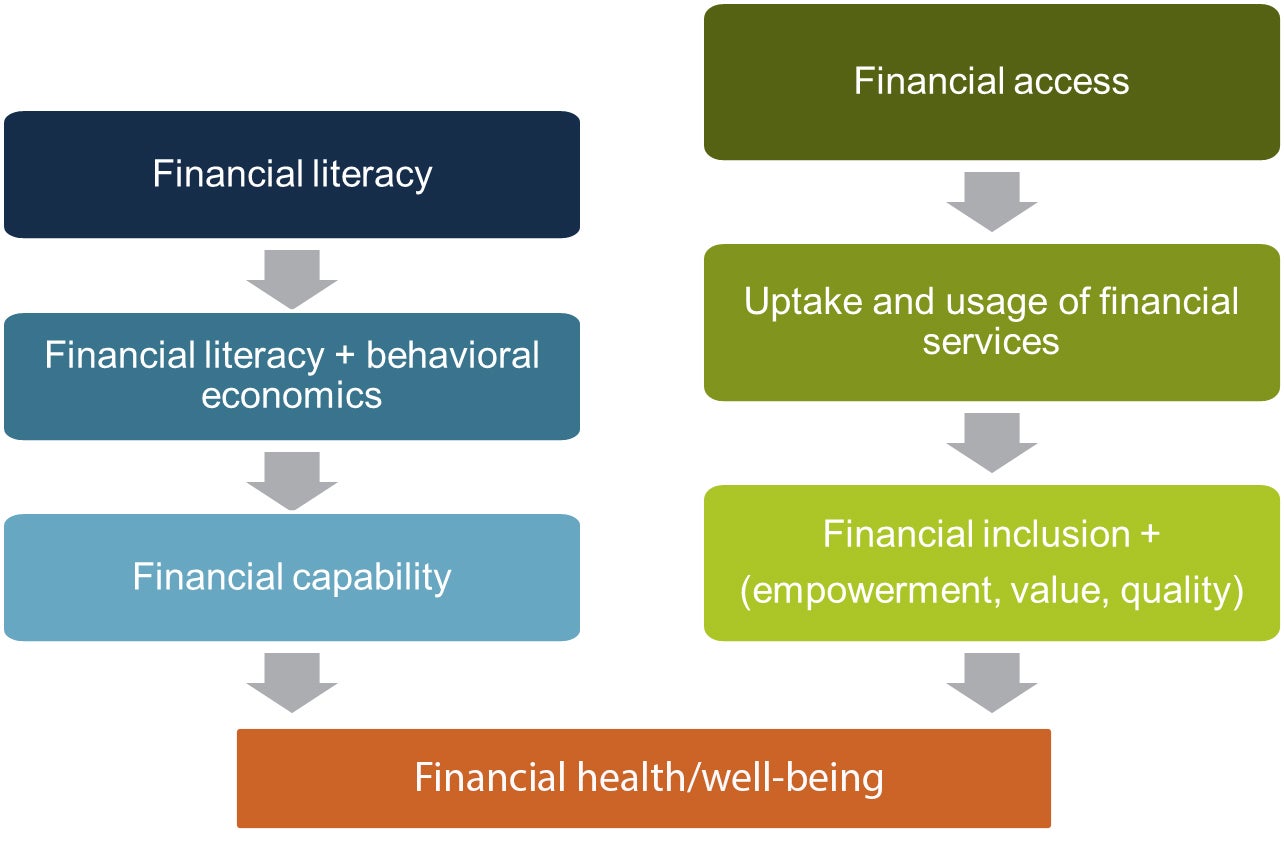

It is important to note that financial inclusion and financial health are not synonymous. When we talk about financial health, we refer to an individual’s circumstances. When we talk about financial inclusion, we refer to a state of the market in which individuals and businesses can access and use a diverse range of appropriate financial services that are responsibly and sustainably provided by formal financial institutions.

Should financial health be the goal of financial inclusion?

Two related fields of work — financial education and financial access — seem to be evolving toward the shared goal of financial health. For example, the need to better evaluate the outcome of financial education programs was a driving factor behind CFPB’s work on financial well-being. CFSI’s work on financial health reflects its view that financial access isn’t the ultimate objective of the financial services sector. In both cases, the concept orients stakeholders around a higher-level goal.

But is financial health a useful concept for those working toward financial inclusion in low- and middle-income countries? After researching the current thinking on these concepts, we certainly see some value in adopting a financial health lens in financial inclusion work. In particular:

- When thinking about how to measure the impact of financial services, financial health is more holistic than simple measurements like increased income or consumption. Financial health tells us more about how people’s lives are changing.

- Financial health offers an alternative and intermediate outcome on the path toward economic advancement. Perhaps improved financial health is a more realistic outcome to strive for and one that might eventually reduce poverty.

- As levels of financial access in low- and middle-income countries rise to near-universal levels, we will need to think about what comes next for financial inclusion. If we only work toward getting people into the system and don’t think about what happens to people once they’re inside, then we really haven’t done our job. Financial health offers one way to orient our work.

- It’s clear that greater access to financial services can have both positive and negative consequences. As Paul Gubbins of FSD Kenya argues, a financial health lens might help ensure we maximize the potential for positive outcomes. It should be embedded in financial inclusion efforts, not seen as an afterthought once access is achieved.

At the same time, the concept of financial health presents some challenges:

- Where would financial health fit into a theory of change for financial inclusion? Financial health is often framed as an intermediate outcome of financial inclusion that can facilitate improved welfare or reduced poverty. Are we assuming that the use of formal financial services inevitably leads to improvements in financial health? Isn’t it possible that financial health is primarily a reflection of a person’s socioeconomic status, not a determinant? If that’s the case, then what do we gain by adding financial health to the theory of change?

- Financial health definitions and measurement frameworks often combine behaviors and outcomes in confusing ways that make the concept less useful. For example, is “planning ahead” — a common element in definitions of financial health — part of what it means to be financially healthy? Or is it a behavior that leads to financial health? You can ask the same question about other elements, such as “using financial services.” Combining behaviors and outcomes makes it difficult to isolate behaviors that are likely to lead to improved financial health. It also assumes that behavior is a key determinant of financial health. Are we putting too much focus on the behavior of poor people? Can low financial health in a population be fixed with changing how poor people behave or does it require changing how markets work? Clearly, both are relevant, but over-emphasizing individuals’ behavior could obscure and distract from structural and systemic factors (e.g., extreme inequality) that constrain opportunities for financial health.

- If we only think about financial inclusion’s impact through changes in people’s financial lives, are we losing sight of the ways in which access to financial services could improve people’s general well-being? Is financial health too narrow?

Financial health has sparked necessary conversations. It prods the financial inclusion sector to think about why we are engaged in this work and what we hope to achieve. Thinking only in terms of number of accounts and dormancy rates can obscure the goal that underpins the sector — improving people’s lives. It also reflects an important evolution in identifying achievable customer outcomes, which we hypothesize could lead to significant progress for providers and regulators working to ensure that financial services provide value to and do not harm vulnerable customers.

At the same time, we’re not sure yet if financial health or financial well-being capture the set of outcomes we hope to achieve through increased financial inclusion. In future blog posts, we’ll share more of our thinking on the links between financial inclusion and financial health and other outcome-based strategies to improve value and protection. In the meantime, please share your thoughts with us in the comments section below.

Related Blogs

Setting Up Funders to Advance Inclusive Finance: 5 Recommendations

Development funders play a key role in advancing inclusive finance – they influence the dynamics of financial systems and transform the way they work to serve people living in poverty. Here, we share five actions funders can take to drive change.

Kickstarting CICO Rural Agent Network Innovation: 5 Tips for Funders

Based on pilots in five countries (Colombia, Cote d’Ivoire, India, Indonesia, Morocco and Pakistan), we share early insights on how funders can engage with stakeholders in Cash-in Cash-out (CICO) rural agent networks to kickstart innovation.

Comments

Interesting and thoughtful…

Interesting and thoughtful piece on financial health, especially where it might fit in to a theory of change. Tricky issues there. How also might it fit in with the SDGs? both concepts in the realm of broad impact level objectives perhaps...

Really nice post, Matthew. …

Really nice post, Matthew. You perfectly articulate the two major concerns that I'm seeing in the body of work on financial health--from one angle it looks too narrow, not fully capturing the broad picture of well-being; and from the other angle it looks to broad and poorly defined. Looking forward to this series!

Regardless of the level of…

Regardless of the level of financial literacy and accessibility, capability, the well-being , sound financial health cannot be guaranteed since later are influenced more by behavioral economics at individual level. To look it through Amartya sen’s lens, there is a difference between perceived behavior and performed behavior . The latter decides the virtual status of financial health.

Mere number of people financially included at output stage does not indicate the well-being unless it is monitored at outcome and impact stage quantitatively

Add new comment