When Clients Inspire Product Design

The Indian microfinance sector has long been criticized for following a one-size-fits-all approach to products and significantly under-investing in innovation. The primary reason for this is a perception that product customization for the poor is a cost, rather than a strategic investment. Similar concerns have been raised about commercial banks’ efforts to further financial inclusion. Approximately 90% of India’s 100 million no-frills accounts —basic bank accounts offered by formal financial institutions lie dormant. This indicates that government and industry initiatives to enhance financial inclusion are unlikely to meet intended results if the focus remains on simply pushing products which are not customized to what the poor need and desire.

Attempting to address this, Grameen Foundation India adopted a human-centered design (HCD) approach to develop a new product for a Karnataka-based microfinance institution, Grameen Financial Services Pvt Ltd (GFSPL). The ultimate goal of this project is to encourage more providers in India to make this transition from a product-centered to a human-centered design approach. You can view Grameen Foundation’s past HCD initiatives here.

Figure 1: Moving from a product-centered to a human-centered design approach

Through this project, we learned about key steps that organizations implementing HCD should incorporate into their projects to optimize chances of success.

Listen to the customer speak in her own voice. We spent two months carrying out extensive field research, meeting clients in their own environment and using various visual tools to facilitate an engaging conversation about their daily routine and map expenses, rather than following a structured Q&A approach. This helped us uncover real client needs that were unmet—for example, we realized that small business owners, who comprise the bulk of GFSPL’s clients, exhibit significant differences in how frequently they need loans, how they use these loans, and how much time they need to repay. Aligning GFSPL’s product suite to these needs would ensure that they did not go to competing organizations for additional funds.

Figure 2: Visual tools to understand customer’s financial saving, borrowing and spending behaviors and help them communicate openly

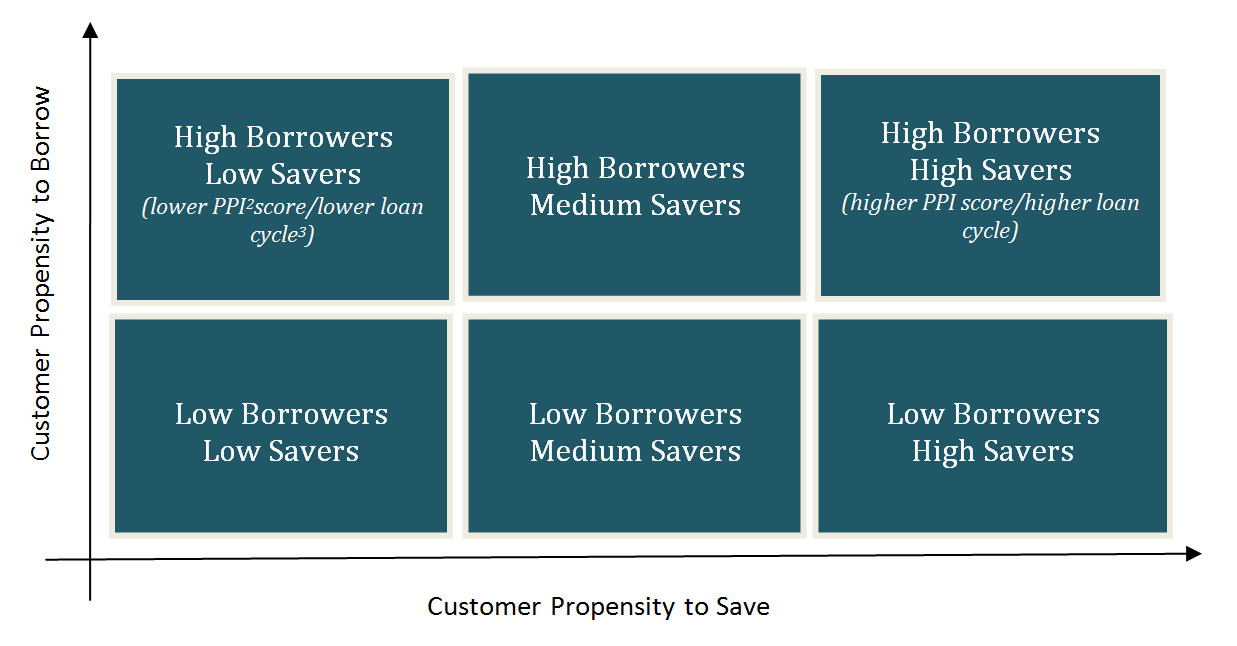

Leverage data that you already have. We synthesized information from our field research and combined it with existing GFSPL data on its clients and their uptake and usage of products to gain insights into drivers of their financial decisions and life events. This exercise helped us map customers based on their propensity to borrow and save, and segment them into six different client personas; each with distinct characteristics, needs and behaviors (see Fig 3). These presented varying levels of innovation opportunities for GFSPL and allowed us to develop an initial list of product ideas. For example: we discovered that high and medium savers have distinctly more complex financial lives; and need flexible, frequent loans. They can however repay in higher installments and at a faster rate, as they typically have multiple sources of income.

Figure 3: Mapping customers on a matrix plotting their propensity to borrow and their propensity to save to discover common dynamics

Field-test ideas early on. We spent a month testing our product concepts—using storyboards and basic prototypes to highlight key features of the user experience for our chosen product ideas to encourage thinking and generate feedback from borrowers and GFSPL staff. This helped us to further refine these ideas, identify risks and translate the early product concepts into more viable ones. For example, after field-testing our final product, we decided to cap the weekly repayments that clients would make in addition to setting an overall credit limit. This would ensure that clients did not borrow beyond their repayment capacity, protecting them and reducing GFSPL’s risk exposure.

Collaborate and co-create. We conducted immersive workshops with GFSPL to collaboratively agree upon initial product ideas, select the final product concept and flesh out detailed product features. GFSPL’s involvement ensured that the product we designed was not only what the customer wanted; but also practical to implement. For example, addressing small business owners’ need for loans aligned with their cash flow needs, our final product solution was a flexible top-up loan option that offered a pre-defined, higher credit limit which eligible customers could utilize via two additional flexible supplementary loans after the base loan. Initially, we planned to call qualifying clients Star Club Members, conferring an achievement-based status on them that others could aspire to. However, we did not proceed with the idea as GFSPL was concerned that this could impact group cohesiveness leading to longer-term repercussions for their lending model.

Address feasibility and viability of product implementation upfront. The goal of user-centered design is to design a product that customers desire, while ensuring its viability and operational feasibility. To ensure that GFSPL’s existing infrastructure was prepared to handle the new product, we integrated it into all existing process maps—identifying pain points, process triggers and roles and responsibilities—and advised on changes that needed to be implemented before roll-out. This also helped us identify process risks early on, and recommend mitigation strategies. We also designed a robust financial model to project the expected business benefits and costs of the new product, allowing GFSPL to make a sound comparison from the current scenario.

GFSPL is now in the process of planning a pilot for this new product. While its commercial success can only be assessed over time, we are glad that this project has institutionalized user feedback at GFSPL. We hope that our experience encourages more financial service providers in India to give clients an active role in their product development efforts; leading to higher adoption and usage rates that ultimately contribute to the achievement of India’s ambitious financial inclusion goals.

Also in this Series

So…What Does HCD Mean for Financial Inclusion?

Human-centered design can help managers understand their customers creatively, iteratively and effectively.

Top 5 Customer Insights from CGAP’s work in Human-Centered Design

CGAP has tried using human-centered design (HCD) to learn from and design better products and services for customers.

Add new comment