Which Way? Mobile Money and Branchless Banking in 2011

There was much movement in 2010 at the intersect of technology and access to finance for the poor. CGAP’s new Branchless Banking Database synthesizes a mass of data into a short 12-image “story” about what branchless banking is and the key hurdles we face in 2011. The focus is on mobile phones, but we quickly add that some of the most interesting work is still being done with debit cards and even simpler technologies, such as bar codes.

Today’s blog starts a three-part series. We first present the latest data about the explosion of mobile ownership in emerging markets and how that converts into an opportunity to boost financial access. The second and third posts will look at performance to date: are we really reaching the poor? Is this proving to be a profitable business for industry? What are the key challenges around products, pricing and channel to pay attention to in the coming year?

Mobile ownership has grown explosively in poor countries over the past decade. In 2005 the mobile phone became the 1st communications device in history to have more users in poor countries than rich. In 2010, mobile phone owners in poor countries accounted for two-thirds of the world’s 4.77 billion phones.

But while people in poor countries became increasingly well-connected via mobile, they remained much less well-connected financially. An emerging market consumer is 2x less likely to have a bank account in their name than own a mobile phone. Access to financial services enables consumers to smooth unpredictable income, acquire productive assets, invest in health and education, and make other purchases that enrich their lives. Fortunately, the explosive pace of mobile connectivity might be leveraged to also fuel financial inclusion.

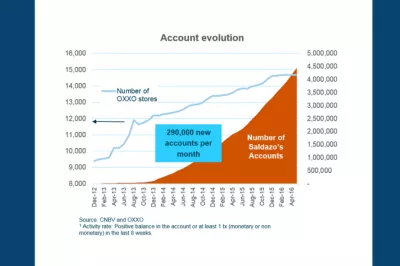

Providers can reap substantial cost savings from channels that replace branches with “branchless banking” (technology paired with agents, typically merchants who handle deposits and withdrawals and are connected via mobile or card-swipe POS terminals). The figure at left shows the cost reduction for 4 Mexican and Colombian banks from moving deposit transactions from teller to agent. Cost savings will vary by institution, driven by inter alia the fixed cost of branch depreciation on one side and variable cost of agent commissions on the other. CGAP estimates most banks will see 50% cost savings or greater. This enables them to reach low-income clients who were previously uneconomical to serve. Other providers — mobile operators, tech firms — which want to enter financial services for the first time can also employ agents to cost-effectively roll out.

Increasingly, financial sector regulators have established enabling regulation for branchless banking. CGAP’s latest analysis is available in two recently published Focus Notes, which build on the scene-setting “Regulating Transformational Branchless Banking”, jointly produced by CGAP and DFID.

CGAP’s Branchless Banking Database is available here. It marshals data from our 2010 field work on agents, business models, customer adoption, and regulation, and combines it with data on banking access, mobile penetration, population, and income in 168 countries. Graphics are easily imported into your own presentations, and the data is presented in Excel, enabling you to manipulate it for your needs.

- Mark Pickens

Related Blogs

")

How Did Bancolombia Create a Successful Rural Agent Network at Scale?

Bancolombia is a great example of a provider that's been successful in developing rural agent business models at scale, therefore playing a critical role in furthering financial inclusion. Here, we look at the factors that explain their success.

Mobile Payments Take Shape in Latin America & the Caribbean

Mobile payments took hold over a decade ago, but Latin America didn't experience the traction seen elsewhere. Since then, two emerging business models for digital payments in Colombia and Haiti achieved particular success. What did they get right?

Add new comment