How Can Licensing Regimes Keep Up with Financial Innovation in 2020?

Newcomers to the regulated financial sector need to apply for a license that fits their proposed business. Licensing categories often define types of regulated institutions, with a range of permitted activities and a set of minimum entry requirements (e.g., initial capital). But with so many new players, are existing licensing categories still adequate? How can regulators know what new categories to create? The way forward is to go back to basics: look at the functions and activities financial institutions perform, and set requirements according to the types and levels of risks associated with those activities.

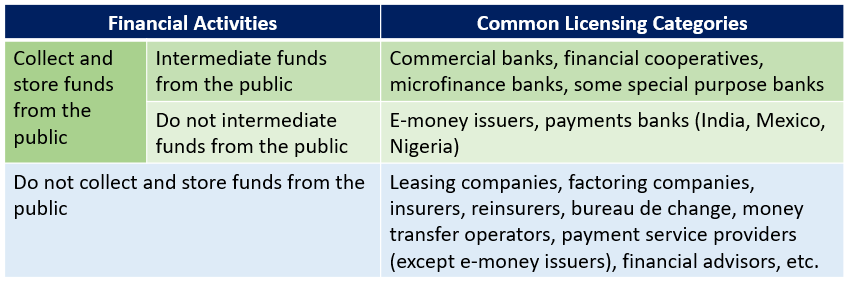

Existing licensing categories broadly divide regulated institutions into those that collect repayable funds from the public (e.g., banks, financial cooperatives, e-money issuers [EMIs], pension funds) and those that don’t (e.g., insurers, payment services providers other than EMIs, leasing companies). Among the former, some intermediate funds in the sense that they make them available to others by offering credits (e.g., banks), while others don’t (e.g., EMIs, pension funds, payments banks).

Existing Licensing Categories for Financial Inclusion

The influx of new players in financial services, which is sure to continue in 2020 and beyond, is making it clear that greater flexibility is needed within these categories.

Take banks, for instance. The commercial bank licensing category offers one of the widest ranges of permitted activities and has a long list of relatively high requirements. However, banks vary in their risk profiles depending on the types of activities they perform — the more activities a bank engages in, the more complex and riskier the bank is. Not all newcomers will engage in all permitted activities, so flexibility in licensing is needed. The requirements for the commercial bank category should not be applied equally across the board.

There are several ways to improve the flexibility of licensing regimes so that requirements placed on financial institutions are commensurate with their activities.

1. Establish tiers within a category

One way is to create tiers within categories based on market segments, size of operations or other factors. In India, for instance, an entrant can choose among two tiers of cooperative bank licenses and six tiers of commercial bank licenses. A potential downside of this approach is that too many and potentially overlapping tiers could confuse newcomers or lead to regulatory arbitrage. There is also the risk that if tiers are too prescriptive, they could steer the market into particular business models, impact profitability, exclude players that do not fit squarely or quickly become obsolete as institutions move to other tiers or categories.

Regulators in Korea, Singapore and Hong Kong have created special tiers for digital banks, and countries like Malaysia are following suit. However, these tiers may have been motivated by broader policy considerations, rather than a strict analysis of risk profiles stemming from the range of permitted activities. An institution under Singapore’s new digital bank tier actually faces stricter requirements than a digital bank created as a subsidiary of an existing bank, which does not fall under the new tier but conducts similar activities. It faces a minimum initial capital of $1.1 billion, while the bank subsidiary needs just $73 million. The high minimum capital has led at least one company to drop its bid for a license.

In Malaysia, there is the opposite situation: the minimum initial capital is lower than for other banks, even though the range of permitted activities is largely the same, which could create room for regulatory arbitrage.

2. Phase in a common set of requirements for all institutions in a category

Another way to add flexibility to licensing regimes is by phasing in the imposition of largely unchanged requirements. The regulator can issue a conditional license, potentially limiting the scope or size of activities until the applicant is able to meet the full requirements. In Singapore, new digital banks do not have to meet the $1.1 billion capital requirement right away. They may start with a reduced capital requirement of $11 million along with significant restrictions on their operational scope. Over time, as the bank demonstrates risk management capability, the limitations are lifted and the capital requirement is increased to the full amount. Australia has a phased authorization for deposit-taking institutions that gives an institution two years to comply with full requirements. Many others, including the Swiss regulator, issue conditional licenses with limitations that persist until a bank can meet full requirements.

3. Customize requirements for each institution within a category

When it comes to regulating digital banks, another approach is to use existing licensing categories for banks but customize requirements based on the combination of activities performed by each bank to reflect their different risk levels. For this to work, the minimum entry requirements for the whole licensing category need to be low enough in the first place. Then, the regulator needs the ability to gradually add requirements. In Europe, where digital banks abound, the minimum initial capital is relatively low, at $5.5 million. When analyzing an application, the European Central Bank estimates the applicant’s required initial and ongoing minimum capital (in addition to the $5.5 million) for the first three years of operation. The result is a customized capital requirement, part of which could be paid up after the license is granted. The Central Bank of Brazil does not have that level of flexibility, but it does have some customization that has benefited new digital banks. The minimum initial capital for banks is $4.1 million (compared to $18 million in Mexico), and pre-established amounts of additional capital (rather than bespoke amounts, as in Europe) apply, according to the types of activities the bank wants to perform.

4. Create new licensing categories

Not all newcomers to the financial services sector are banks, but some might engage in activities included in the bank licensing category. An example is EMIs, which collect repayable funds but do not extend credit, making a case for a nonbank licensing category. (India, Mexico and Nigeria are the exceptions, as they have bank categories for this type of business.) In addition to EMIs, other emerging businesses may not fit the existing licensing categories even if there is flexibility for the customized imposition of requirements.

Overly restrictive licensing requirements can impede competition, while excessively lax licensing can put systems and consumers at risk. Regulators should increase flexibility in their licensing to accommodate innovation but keep risks at bay. They must make an effort to be more sensitive to the levels and types of risks and activities of individual entrants. As rightly stated by Christina Segal-Knowles of the Bank of England in the context of regulating payments, “We need to move away from a system in which how you are regulated depends on the type of entity you are, towards one in which what matters is the risks you pose.”

Add new comment