BNPL in Nigeria: Emerging Fintech Innovations for MSEs

Adebisi, a peri-urban micro retailer in Nigeria, has struggled to grow and expand her business for years as she’s had to rely exclusively on financing from family and friends. However, the recent proliferation of fintechs that provide inventory financing and logistics support for delivery of her purchased stock have gone a long way in solving her most pressing business challenges. Adebisi now uses a fintech that offers buy now pay later (BNPL) services for inventory finance to restock her goods weekly. She orders the goods from the comfort of her store and gets them delivered directly to her on credit, which she repays within the month. She is now able to buy an additional 30% of stock, compared to her previous purchases.

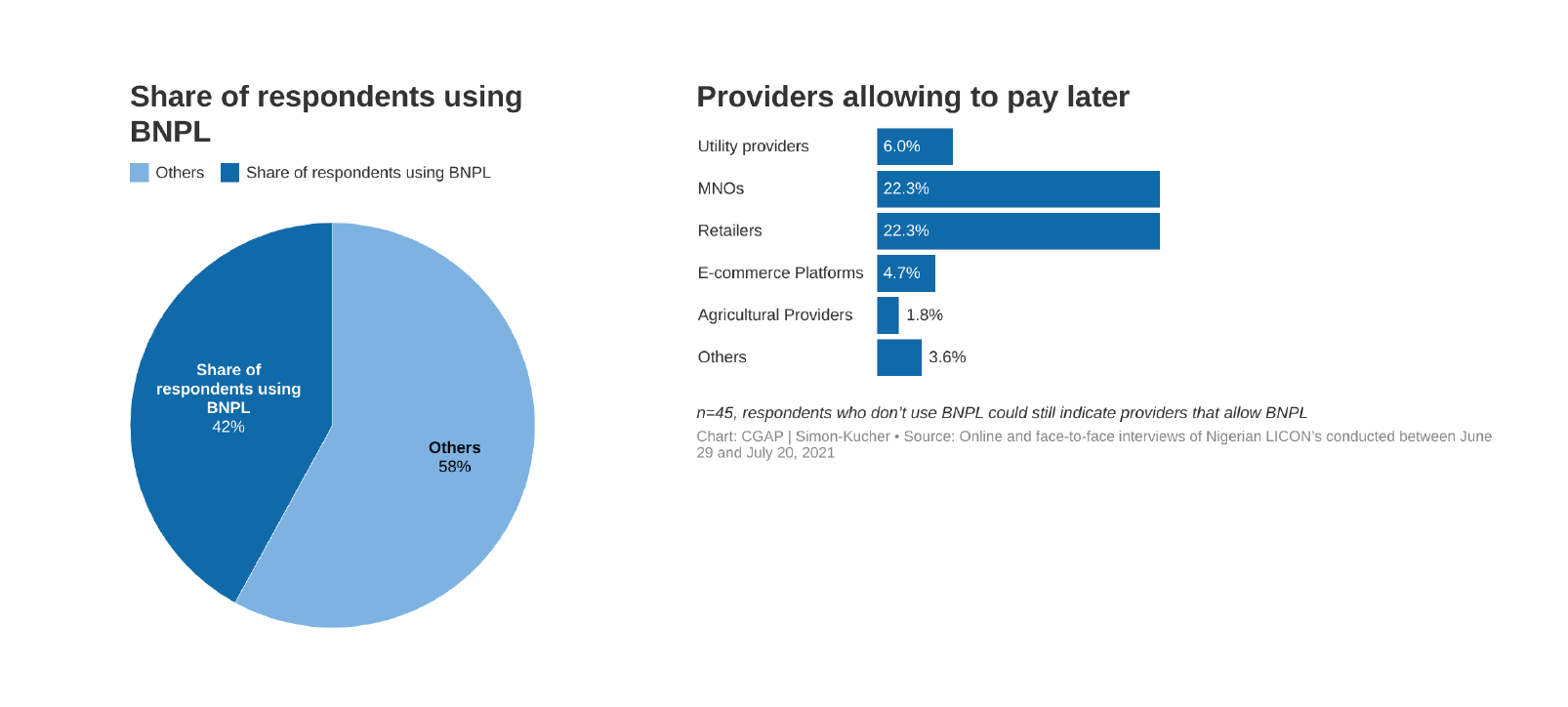

Adebisi is just one among many self-employed and micro/small business owners benefitting from a suite of BNPL products available through new fintechs that use digital data trails to provide finance to those excluded and underserved in the past. Findings from a CGAP-commissioned research initiative in 2021 suggest a growing trend in the Nigerian BNPL space, with BNPL becoming a significant lending mechanism for Nigerians – especially micro, small and medium enterprises (MSMEs) and self-employed individuals who would not otherwise have access to credit. The research estimated the size of the micro and small enterprise (MSE) and low-income credit markets in Nigeria and assessed the potential of fintech firms to meet the needs of those markets. The resulting report revealed that BNPL is the largest credit source for MSEs in Nigeria, as wholesalers are most likely to provide BNPL services to MSEs.

Traditional providers find it challenging to serve MSEs due to a variety of factors, one of which is their lack of data and low digitization rate

Although lending is perceived to be profitable for financial services providers (FSPs) in Nigeria, the incumbents still shy away from lending to MSEs, a segment that is increasingly gaining the attention of Nigerian-based fintechs. MSEs face various challenges in accessing the different financial services available in the market. Many MSEs do not maintain detailed records of their business activities, which means they lack the requisite data and necessary documentation, collateral and financial records that are needed to access formal financial services. These gaps and their low digitization rate make MSEs unattractive to banks. The high level of informality of the MSE space, its fragmentation and cash-based operations lead to these pronounced issues — a high cost to serve, data asymmetry and the inability of traditional financial service providers to extend credit.

The Global Findex Database 2021 has shown that low-income groups are less likely to be able to use banking services confidently, which could explain why fintechs are going a step further to support MSEs (especially those run by women) in the use of digital lending products being offered.

Fintechs have a strong positioning to provide innovative financial services to MSEs

The fintech market in Nigeria is fast-growing and thriving, with more than 250 providers, about half of whom are providing payments services. While there has been a long-time focus on payments among Nigerian fintechs, there is now a gradual shift to lending as well, especially in the Fast-Moving Consumer Goods (FMCG) value chain. About 15% of Nigerian fintechs are now focused on lending to SMEs. In 2021, BNPL accounted for close to half of the total credit volume disbursed to MSEs, according to CGAP-commissioned research.

While the BNPL model is considered an emerging form of credit for MSEs, and data from the research shows a rise in the use of BNPL in Nigeria, this type of credit has actually been in use in the country for quite some time, if not just in different forms. The model has always varied from wholesalers giving goods to retailers on credit with specific repayment terms, to large distributors of tech gadgets like Samsung partnering with FSPs to facilitate BNPL services to FSP customers. So, what is different about the current BNPL models? Fintechs are now able to offer BNPL at scale and more efficiently by leveraging digital data trails. These fintechs are digitizing supply chains (or parts thereof) by using customer data to offer BNPL services, thus addressing the gaps in the older, informal BNPL models that were largely based on trust alone. This is because, in general, fintech entrepreneurs are seen to be more comfortable lending against inventory or assets (as opposed to disbursing cash loans) to reduce the risk of fund diversion to undisclosed or unproductive ventures and assets.

The emerging Fintech-led BNPL products that serve MSEs come in different forms and serve different MSE needs

BNPL for inventory or stock to MSEs

There are various BNPL models in Nigeria, each of which distinguishes itself by the types of products and services offered - these typically fall into two buckets. On one hand, there are fintechs that offer BNPL for inventory or stock to MSEs. These are usually small loans in the form of inventory which are repayable partially or in full within an agreed-upon period. There are now a growing number of fintechs offering business-to-business (B2B) working capital solutions to MSEs in the FMCG industry.

These fintechs link retailers to their suppliers while providing inventory and embedded finance solutions to help MSEs buy more stock and expand their businesses. Some of the fintechs running these models go a step further by providing logistics support and stock delivery to the retailers, thus offering MSEs the convenience of ordering from their shops, time savings, reduced transport costs and, in most cases, improved margins as a result of discounted prices. Some even provide goods on consignment or offer retail business analytics based on historical data and data from similar businesses in the area.

Through digitized BNPL models, these fintechs are developing digital data trails that help MSEs build credit histories that enable credit scoring. The process is more seamless when the MSEs can order stock and apply for inventory financing digitally from their smartphones. A good example of this is Boost, a Nigerian fintech that enables retailers, particularly women, to make stock orders digitally via WhatsApp and uses retailers' order data to provide working capital to the retailers to unlock missed sales and grow their margin. This model involves Boost receiving the stock orders from these women, placing orders with the wholesalers and then distributing the stocks to the women retailers.

BNPL for productive assets or consumer goods to MSEs/individuals

On another hand, there are fintechs that offer BNPL for productive assets or consumer goods to MSEs/individuals. This model leverages simple credit scoring based on basic customer demographics and data. For repeat customers, the models rely heavily on their lending and repayment history. For first-time customers, models will use customer demographic data and other self-reported data. Among consumers, BNPL enables the purchase of consumer goods such as food, clothing, airtime and gadgets such as phones and electronics. For MSEs, this model is useful in acquiring productive assets required to start and/or grow their business.

An example of this model is Altara, a fintech that operates in peri-urban and rural centers in Nigeria offering BNPL to both individuals and MSEs, enabling them to access inventory and other assets like smartphones, refrigerators, generators, freezers, etc. Interestingly, Altara has discovered that low-income customers who take out an initial smartphone loan tend to subsequently apply for a loan for a productive asset or stock to either start a new business or support and grow an existing business. While Altara uses financial data leveraging banks’ APIs and other secure/reliable open banking infrastructure offered by some fintechs for its already-banked customers, it uses demographic data for most of its unbanked customers for improved customer understanding.

The two BNPL models highlighted demonstrate the wide variations in terms of cooperation with other supply chain actors depending on how the purchasing and pre-financing, storage, transportation and payment of the goods are organized. This ranges from pure-play models, often capital and asset-heavy, where the fintech takes care of the entire process, to embedded models where different players are involved throughout. What they all have in common is that they offer (near) instant and unsecured loans in the form of inventory/assets, underwritten through some form of a data-based credit decisioning model.

Providing these innovative and tech-driven services hasn’t been easy for fintechs as they face various challenges within the ecosystem. For example, Nigeria is considered to be the largest mobile market in Sub-Saharan Africa but lacks infrastructure and connectivity in the country's rural areas – where many MSEs and low-income consumers are based. BNPL is clearly going to continue to be a mainstay of finance in Nigeria, providing access to the likes of Adebisi and many others like her, giving them a chance at improved livelihoods. It will be critical that providers — and especially fintechs — can rely on a stable enabling environment to support more innovation and sustainable growth, keeping these customers’ needs at the heart of their business.

Related Blogs

African Digital Credit Goes West

Digital credit is emerging in West Africa. Despite early reports of low default rates, consumer protection policies will be key to avoiding problems witnessed in East Africa.

Client Registration: The Blind Spot in Agricultural Insurance

This agricultural insurance provider tripled its product registration rates in rural Nigeria by improving its registration process.

Add new comment