Maximizing the Impact of Financial Inclusion for Young Women

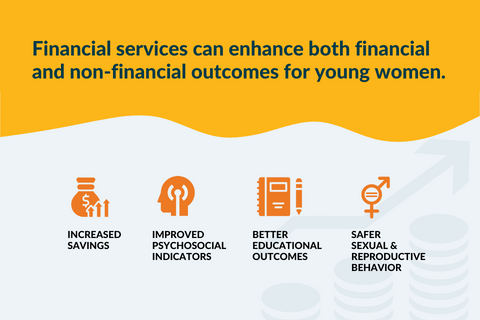

Research has shown that financial inclusion can contribute to improvements in both financial and non-financial outcomes for young women. However, the ~590 million young women in the world (defined as women ages 15-24) are a tremendously diverse group, transitioning through different life stages within vastly different contexts. Considering these differences, among which segments of young women could improved financial services make the most impact?

Multifaceted marginalization calls for a multifaceted response

Globally, young women remain one of the most marginalized financial service client segments. Despite improvements over the last several decades, young women ages 15-24 still have lower literacy rates, higher HIV rates, and lower labor force participation than their male peers. In addition, CGAP’s social exclusion analysis found women faced the highest levels of exclusion from markets, services, and spaces of any segment of financial service users. Young women’s adoption of financial services also levels off far earlier than young men’s, producing a pervasive gender gap in financial inclusion.

To address the multifaceted nature of young women’s marginalization, an arsenal of programmatic interventions has been developed, often combining interventions across multiple sectors. Educational interventions and job training aim to increase young women’s economic potential, and sexual/reproductive health programs seek to delay childbearing and reduce unsafe sexual practices – impacting health and fertility at both the individual and community levels.

Although they receive less focus, financial services – including savings and lending groups, savings accounts, and business loans – are also common ingredients in programs designed to improve well-being outcomes for young women. Over the last decade, several evaluations have documented increases in young women’s savings as a result of such interventions. Others have shown how a financial inclusion component can enhance the impact of educational, health, and psychosocial interventions, directly or by increasing participant fidelity to the program.

While this research is promising, efforts to translate findings into actionable guidance for funders, program designers, and implementers have been challenged by two gaps. To date, there has not been a comprehensive attempt to pull together the impact evidence to understand which financial inclusion approaches have yielded consistent results for young women or how to scale them. This task is also complicated by the level of diversity within this segment. Young women between 15 and 24 include students and workers; may be married, single, and/or mothers; and live in vastly different cultural contexts, where they face both shared and unique forms of marginalization.

Understanding this diversity is critical not only to parsing the research, but also to developing a strategic sense of for which segments of young women investments in improved financial services might yield the most impact. To accomplish this, CGAP commissioned Kore Global and Driven Data to conduct a segmentation that examined this question from three angles, and we have shared these results in a new infographic and related video.

- Segment size, conceptualized in terms of life stage and context

- The prevalence of needs that research has shown can be addressed by financial inclusion

- The “relevance” of financial services; i.e., the extent of barriers faced by a given segment that would affect the likelihood of impact

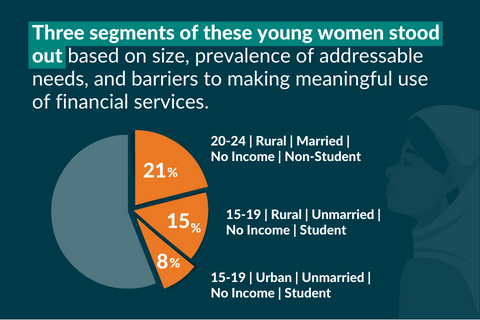

As a global dataset did not exist, we chose four illustrative countries: Bangladesh, India, Kenya, and Nigeria – together home to more than a quarter of the world’s 590 million young women in this age bracket. Data came from the latest available FII datasets (for 2017-18). The results were illuminating:

The largest segments of marginalized young women are rural, with no income

Over one-fifth of the total number of young women in our analysis were 20-24 years old, rural, married, with no income of their own (“at-homes”). Another 15% were rural students ages 15-19, while 8% were their urban counterparts. Across the segmentation, being in school correlated with being unmarried; married students made up less than about 2% of the total. And, like 80% of the total population studied, the vast majority of full-time students reported having no income.

Needs are widespread across this group, but especially high among younger segments

As this exercise studied economically marginalized young women, it is not surprising that only one segment in one country qualified as having “economic agency” per the FII’s definition. But even within this group, younger segments displayed lower personal financial health, with many coming from households living on less than $1.25/day, and very few reporting saving within the last 90 days.

Relevance measures varied more by country than by segment

This attests to the importance of national context in determining barriers to financial inclusion. This was especially true with regard to possession of a national ID (almost universal in India, but as low as 7% among younger segments in other countries) and awareness of nearby mobile money agents (upwards of 85% across segments in Bangladesh but topping out at 30% in Nigeria). Other dimensions of relevance were surprisingly consistent across both segments and countries. Numeracy, for example, was universally high, while financial capability was universally low. Perhaps most intriguingly from a program design perspective, while respondents didn’t necessarily own a mobile phone or SIM, almost all reported knowing how to use a mobile phone.

Where does all this information point us?

Potentially, in the direction of younger rural students. While not the largest single segment, 15–19-year-old rural students make up 15% of the total across these four countries. Needs in this group are also significant – their economic agency scores were often the lowest of any segment, and less than a quarter in any country had emergency funds. In Bangladesh, Kenya, and Nigeria, only 7-16% had any kind of financial account. Conversely, depending on the country, rates of SIM ownership in this segment – as well as their proximity to bank branches and, most importantly, school-going status – make them potentially reachable through various program delivery channels. Finally, younger rural students share important characteristics in common with the first and third segments by size (older, rural, married “at-homes” and younger, urban students, respectively) – meaning that addressing their barriers may be beneficial for all three segments.

Over the next three years, CGAP will be building on this hypothesis by sharing more specific guidance on how to maximize the impact of financial inclusion for young women. In 2023, we anticipate publishing a systematic review of impact literature in this area (currently being conducted by Global Social Development Innovations) summarizing what types of financial inclusion interventions have produced proven outcomes for different segments of young women. We will also be convening a consortium of practitioner organizations to distill the operational wisdom underpinning successful program implementation. Future efforts will be devoted to more granular market research, risk analysis, and ultimately pilot projects that seek to scale the impact of proven approaches.

We know the multifaceted nature of young women’s marginalization requires a multifaceted approach. So, we are looking for collaborators working on either financial inclusion or young women’s development – or both – in the areas of financial services, broader support programming, market research, and policy. If your organization is interested in partnering on any of the above, please get in touch!

Add new comment