Surveys Reveal a Path to Responsible Digital Finance in WAEMU

While digital finance services have lowered costs across the board and improved convenience for customers, they introduce new risks that can negatively impact consumers’ lives. Findex 2021 data shows some concerning data in terms of consumer protection, and CGAP’s 2022 global research on the evolution of the nature and scale of digital finance consumer risks found increasing types and frequency of frauds and consumer data misuse – confirmed by the recent OECD Consumer Finance Risk Monitor and the Consumers International Fair Digital Finance Index.

This underscores the urgency to better monitor consumer risks and foster more responsible digital finance, especially in countries with fast-growing sectors. In this spirit, CGAP launched the WAEMU Digital Finance Services Consumer Protection Lab (the WAEMU Lab) in 2021. The Lab aims to make digital finance services in the region more responsible, reducing consumer risks and ensuring value.

Working closely with local and regional authorities, in particular the Observatories for the Quality of Financial Services, CGAP conducted national phone surveys on consumers' experience and exposure to DFS risks in Cote d’Ivoire, Senegal, and Burkina Faso. In all three countries, the primary use of digital finance is transfers and payments via mobile money.

Digital finance is not yet available for all

CGAP found a 10 to 30 percentage point gap between usage by women and men, and a major “urban bias” in all countries, with only 15% of mobile money users residing in rural areas in Côte d’Ivoire, for example.

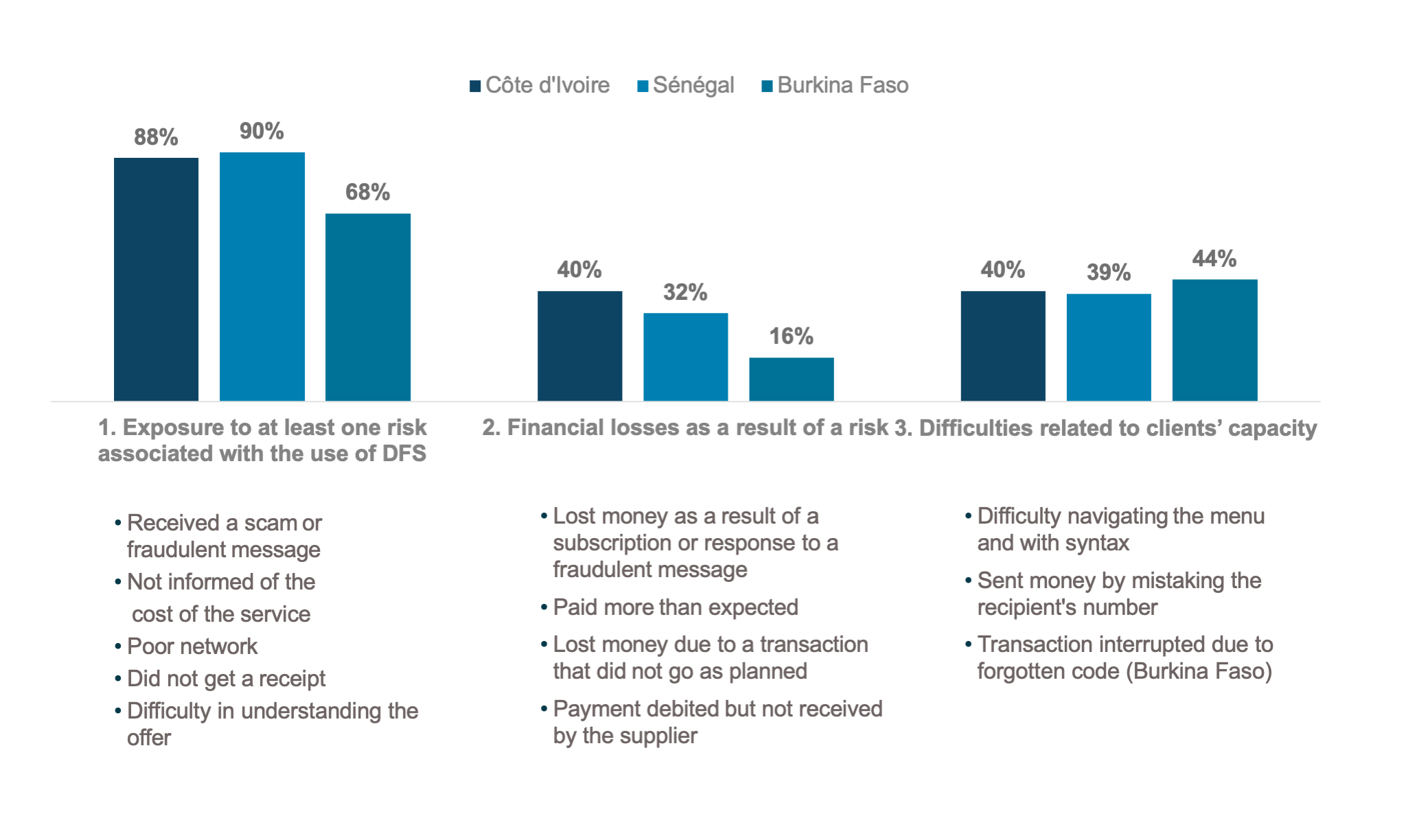

Users of DFS face significant challenges in the three countries surveyed

Depending on the country, the surveys showed that between 68% and 90% of users faced risks from using DFS in the past year. These risks have led to financial loss for a large proportion of users in Senegal and Cote d’Ivoire (32% and 40% respectively), but less so in Burkina Faso (16%). In all three countries, the surveys show significant challenges for almost 40% of users to make transactions properly.

Exposure to fraud is a major concern in Senegal and Côte d’Ivoire

The lack of transparency is also concerning, with 55% (Senegal) and 33% (Côte d’Ivoire) of users not having been informed of the cost of the service before carrying out a transaction. These risks are lower in Burkina Faso.

Recourse mechanisms vary widely from one country to the other

While Burkina Faso stands out for its high rate of customer service use (84%) and problem resolution (94%), in Côte d'Ivoire and Senegal, complaint resolution is lower. In Côte d'Ivoire, 33% of users contact customer service with 72% resolution, and in Senegal, 47% contact customer service with 86% resolution.

Agents don’t always have liquidity but they can help consumers to transact

Agents tend to play a positive role in helping consumers understand the services, but they do not always have the liquidity needed for consumers to cash out. In Cote d’Ivoire, they warn consumers against potential fraud, but the surveys also showed significant issues in terms of availability of liquidity.

"There are customers who come from distant villages to withdraw money in the locality and be able to meet their daily expenses…but the agent tells them there's no more money, whereas he only needs 15,000 FCFA (approx. $25) to meet his needs.” - Mobile money user in Niakhar, Senegal

Poor GSM network, preventing smooth transactions, and exposing users to money losses, is a feature common to all three countries. In Côte d’Ivoire, Senegal, and Burkina Faso, 61% (Côte d’Ivoire), 44% (Senegal), and 55% (Burkina Faso) of DFS users faced this challenge at least one time in the past twelve months.

Surprisingly, significant gender differences in overall risk exposure were rarely observed

Throughout the surveys, we looked for gender-disaggregated data, predicting that women would be much more exposed to risks than men. However, the results were not as clear as expected and called for some nuance. For example, in the three countries surveyed, we found no significant gender differences in risk exposure or capacity-related difficulties in using DFS, but women reported needing more help than men to use the services.

One woman consumer interviewed by CGAP in a small city in Burkina Faso said: “For a better use of their mobile accounts, women should be trained and sensitized about the need to keep their pin secret.”

Gender gaps do exist for specific risks. Women made fewer recipient or amount errors (6-7% gap) as they are more likely to seek help and often use a single account. However, women had more difficulty navigating menus and using USSD syntax, which is consistent with the fact that women are more likely to seek help in using services.

Another surprising result in all three countries is that women did not strongly prefer transactions with agents of the same sex, with only 4-12% expressing this preference.

The survey results have triggered many initiatives that will contribute to more responsible DFS

These national surveys shed light on the urgency to ensure that DFS leads to better experiences and outcomes for consumers in the region. They have also prompted collaboration among diverse stakeholders within each country's digital finance ecosystem, prompting concrete actions:

- Financial sector authorities of each country (e.g. agencies within the ministry of finance) have developed action plans to reduce consumer risks in consultation with other digital finance stakeholders. In Cote d’Ivoire, for example, the OQSF developed a price comparator to improve mobile money pricing transparency and a video for the public to alert against DFS fraud.

- Digital finance providers in Senegal and Cote d’Ivoire, like MTN, Orange, and Wave, are stepping up their efforts to fight fraud which is particularly high in both countries. OQSF and providers also conducted awareness campaigns in Senegal to fight fraud and scams.

- International funders are supporting more responsible practices in these three countries and beyond. The US Trade Commission has organized capacity building for regulators, and the World Bank is supporting Niger to launch a similar national survey.

- Finally, at the regional level, the Central Bank of West African States (BCEAO) is reviewing the regulatory framework for consumer protection in financial services, including DFS.

Ultimately, the WAEMU Lab will only be successful if DFS users face fewer risks and get what they expect from the services they purchase. We can only know this by monitoring the situation on the ground. In Côte d’Ivoire, the Lab is supporting local authorities to monitor the evolution of consumer risks and experience with a follow-up survey. The results will tell us if risks have decreased since the first survey undertaken in 2022.

Related Blogs

Digital Credit in Côte d'Ivoire: A Double-Edged Service

Digital credit can provide opportunities for financial inclusion and improved resilience, but new survey data from Côte d'Ivoire shows the need for greater consumer protection.

Growth of Digital Finance in Côte d’Ivoire is Not Without Risks

While digital financial services are driving financial inclusion in Côte d’Ivoire, we are also seeing the emergence of significant consumer risks that will require concerted action from all stakeholders in the digital finance ecosystem to counteract.

Add new comment