Cashless & Cashy: The Yin-Yang of Digital Delivery in Peru

Financial services innovators in Peru may have secretly adopted Chinese philosophy.

When it comes to delivering financial services to lower income segments, these innovators have struck an interesting balance between cashless and cashy transactions – sort of the yin-yang of agent networks– as they built synergies across services, rather than following an either-or approach.

According to the latest CGAP research on branchless delivery in Peru, cashy transactions, which are cash-based over-the-counter transactions such as bill payments, represent a significantly large transaction pool for agent networks, ranging from 40% to 90% of their total income. Therefore, these cashy transactions are a fundamental factor that helps determine the viability of agents. Here’s how.

In rural areas transaction volumes are lower than in cities, which makes it harder for agents to break even. Cashy over-the-counter transactions are often criticized for having little financial inclusion benefit. However, in the case of Peru, cashy transactions are enabling agents to operate viably in areas where they would have otherwise failed. The sheer volume of demand for cashy transactions helps cover the agents’ operational costs and thus powers agents’ services – cashless or otherwise. Without offering cashy services, many rural agents simply could not afford to exist.

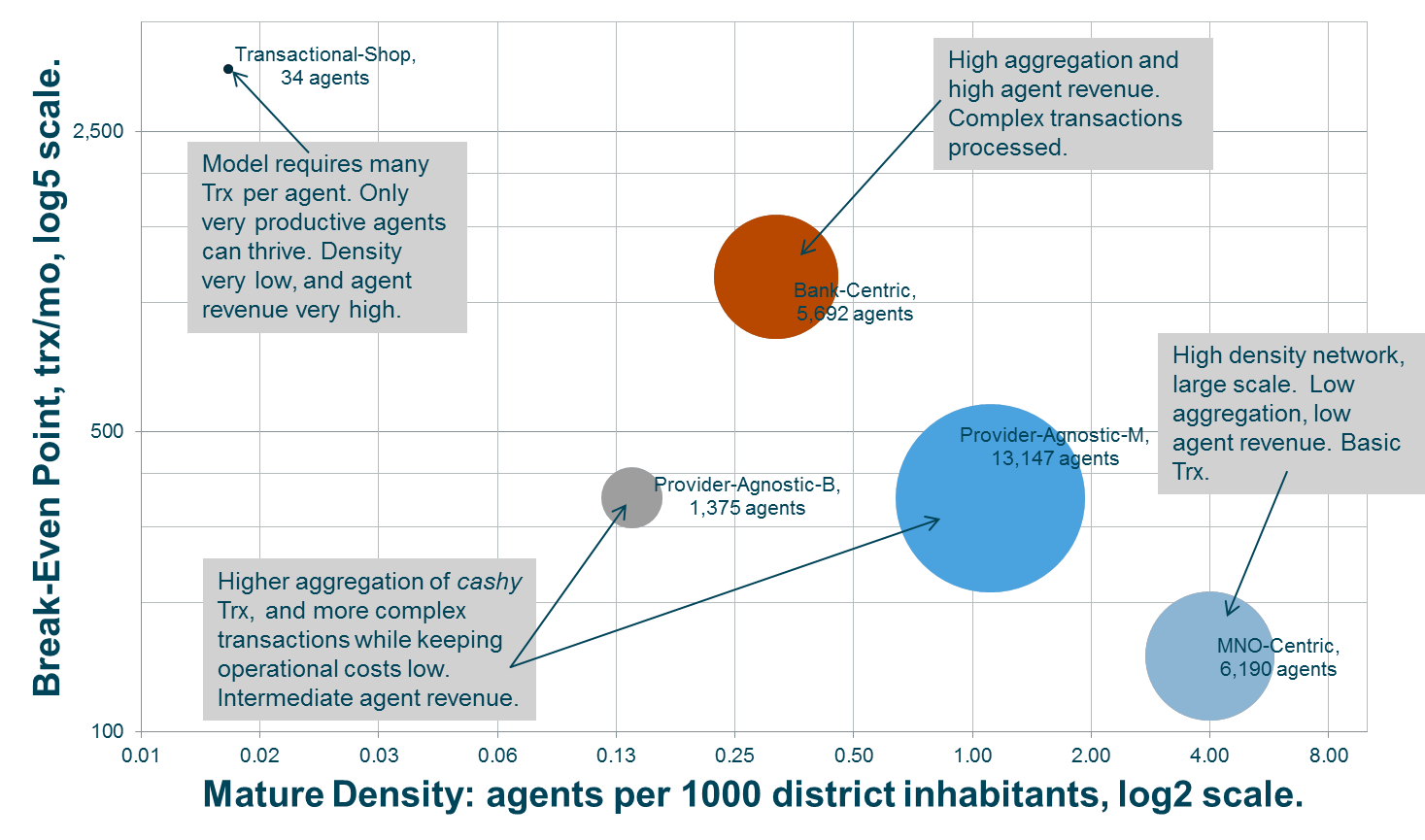

The Peruvian experience shows that aggregation of both cashy and cashless account-based services, such as digital financial services, is a key driver for agent revenue: the more services offered, the larger the transactional pool that can be tapped by an agent. Highly aggregated portfolios display up to eight times more agent revenue than some exclusive single provider portfolios. The study found that agent networks with simpler transactions display increased agent density per locality, both in rural and urban settings. Transactions that involve more expensive infrastructure, such as those needing to follow more complex procedures or comply with steeper regulatory requirements, limit the number of agents that can reach Break-Even Point (BEP) in a given area. Primarily, this implies that service complexity limits ability to drive presence in rural localities. Business models studied range from 3500 to 150 monthly transactions for BEP.

While cashy transactions, aggregation of services and simplicity are the key drivers of dense and large scale agent networks in Peru, there are tradeoffs between these factors. For example, while simpler cashy transactions provide lower break-even points and denser networks, their financial inclusion potential is more limited. At the other end of the spectrum, aggregation of more complex financial services which require for example paper receipts, would raise break even points and could make agents unsustainable in areas where transactions are scarcer.

Consequently, there is a sweet spot for developing large scale and dense networks that are also viable in rural areas. The Peruvian experience highlights the importance of striking the right balance between keeping agent break-even points low while providing both a variety of services and strong financial inclusion and customer protection benefits.

About the research

This study on branchless delivery encompassed the characterization of five agent networks in Peru, with more than 26,000 agents and 24 million monthly transactions in total. Agent networks participating in the study provided detailed operational data. The four main types of networks identified in the Peruvian market were: Bank-Centric, MNO-Centric, Provider-Agnostic and Transactional-Shop.

The study provides as well some interesting insight for the financial inclusion debate in other markets, developed further in the accompanying slide deck and brief:

- Rural coverage: aggregation, especially of cashy transactional pools, together with simplicity in order to keep operational break-even points low, are key elements for viable agents in rural areas.

- Regulation: optimal balance between simplicity and operational requirements for banking services offered through agents, would increase scale and density of the networks both in urban and rural settings.

- Interoperability: aggregation from third party agent networks can be an easier alternative to interoperability as it enables over the counter transactions between platforms but it that does not require interconnection at the service provider level.

- Tiered agents: both for operational and regulatory purposes the idea of establishing tiers of agent, which is already being implemented by some operators, can be useful to enable network density and scale across distinct geographical areas.

Resources

Related Blogs

Five Lessons about Agent Networks in Peru

CGAP recently completed a study of five agent networks in Peru comprising more than 26,000 agents and 24 million monthly transactions to identify key success factors in reaching poor and rural areas.

Can Agents Improve Conditional Cash Transfers in Peru?

Innovations for Poverty Action is working with the Peruvian Government to test conditional cash transfer programs that help poor people save more and receive their payments in more convenient ways.

Add new comment