Responsible Digital Credit for Merchants: Insights from Kenya

As digital credit expands rapidly in East Africa and elsewhere, offering credit responsibly, including to merchants, is becoming increasingly important. Meeting legitimate credit needs, while avoiding over-indebtedness and other detrimental outcomes of credit, requires good understanding of the market and borrowers. In Kenya, CGAP recently partnered with Kopo Kopo to better understand merchants’ experiences with Grow, Kopo Kopo’s cash advance offering for merchants who use its transaction payments platform. Grow is unique in that merchants repay their advances as a percentage of the digital transactions they receive on Kopo Kopo’s payment platform. In this way, merchants are not on the hook for set weekly or monthly payments, which is especially helpful when business is slow.

Kopo Kopo wanted to better understand what aspects of the advance were working well, as well as any problems or risks that merchants were experiencing in order to offer the advances in an even more merchant-friendly and responsible way. Our mixed-methods study with Kopo Kopo and the Busara Center for Behavioral Research, which included analyzing transaction data from hundreds of merchants who had taken out a Grow advance and dozens of interviews, revealed some characteristics of Kenyan merchants that would be useful to anyone trying to expand merchants’ access to credit in a way that benefits both the lenders and the merchants.

Merchants often combine credit sources and use digital credit to augment other loans

Nearly all of the merchants we interviewed were balancing multiple credit sources simultaneously, including sources like bank loans, bank overdrafts, SACCOs, M-Shwari and Grow. There was an overarching belief that a smart businessperson should take credit whenever it is available, as a need will always arise.

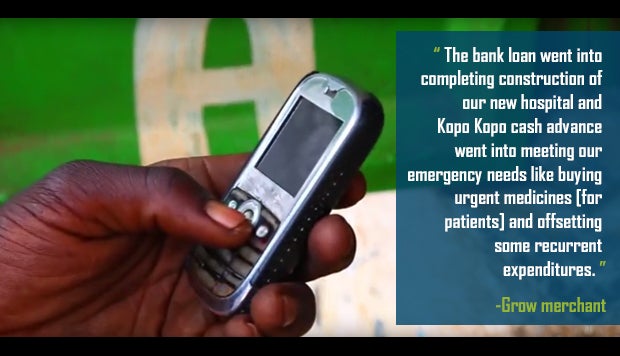

Most viewed Grow as complementary to, rather than a substitute for, other credit sources. Merchants appreciated the speed, efficiency and flexibility of the Grow advances, though they said its fees were higher than most other sources. For some merchants, the combination of high speed and increased cost made Grow a “premium” source of credit to be used selectively. For example, many merchants said they used Grow advances in cases of emergency, when they needed funds quickly, and were willing to pay the higher cost. Others used it to “top-up” bank loans that were not large enough, and others used it to meet recurring expenses such as salaries or inventory when cash flow was insufficient. Merchants also liked Grow’s unique and flexible repayment model. As one merchant said, “[With] Grow, you hardly feel the burden of paying the [advance].”

Merchants change behaviors as a result of digital credit

Transaction data shows that merchants push digital transactions with their customers in order to improve their credit qualifications. Transaction volumes spiked one month prior to a merchant taking out an advance — on average, there was double the transaction volume compared to the three months prior to an advance — likely because merchants hoped to qualify for a larger advance. In addition, the vast majority of advances were repaid faster than expected, indicating that merchants are encouraging customers to use the Kopo Kopo transaction platform in order to pay off advances more quickly. The rapid repayment is evident across all merchant sectors, geographies and tenures with Kopo Kopo.

Reuptake is also very quick. The median time between Grow advances for repeat merchants is just three days. Merchants cannot take out a new advance until they have paid off their existing Grow advance, so it is very likely that merchants are repaying fast to gain access to their next advance.

Here the data are at odds with what merchants reported in their interviews. While merchants generally said that Grow is a relatively expensive source of credit that they only use for emergencies or specific circumstances, their rapid reuptake suggests that they often use the advances as a continual line of credit.

Merchants tend to borrow the maximum amount available

In addition, the study suggests that merchants may not be making active decisions about the size of the advance they need, but taking the maximum amount they qualify for. When they do consider alternative amounts, the focus is only on how much they think they can repay, rather than on the expected return from the use of the advance. Some seemed confused that they even had a choice on advance size. According to one merchant, “I did not decide [the size of my advance]. The system generated the amount automatically.”

Considerations for digital lenders

Taking out many advances in quick succession, and taking out advances without considering the cost and likely return, could be problematic for merchants’ long-term business prospects. Helping merchants make good credit decisions is beneficial both for the merchant and the credit provider. The merchant can maintain an available line of credit, and the credit provider can avoid over-indebtedness and possible default among its borrowers. The findings from this study point to a number of actions that Kopo Kopo and other digital lenders can consider when offering loans:

- Encourage active decision making by merchants when they decide whether and how large of an advance to take out.

- Encourage merchants to plan how they will use the advance and compare the likely return to the cost of the advance.

- Maintain good understanding among borrowers of fees, repayment requirements, consequences of late or non-repayment, and other terms, such as through effective disclosures.

- Use website analytics (or other platform analytics) to understand which parts of the website merchants click on, understand how much time they spend on each, and improve the interface to encourage planning and understanding of terms.

Expanding access to credit for merchants can be a win-win for merchants and lenders if done well, and insights like these give an indication of how to embed good practices in the rapidly evolving digital credit market.

Related Blogs

The Wrong Kind of Credit: Why Loans to Gig Workers Must Reflect Income

Volatile gig income and inflexible loan repayment schedules can be a dangerous mix, as this ride-hailing driver in Nairobi learned from experience. His story serves as a cautionary tale to lenders and borrowers in the gig economy.

Kenya’s Expansion of G2P Becomes Lifeline During COVID-19 Crisis

Kenya offers higher fees to providers that facilitate digital government-to-person payments in underserved areas. Today, this makes it easier to reach hundreds of thousands of low-income people with assistance during the COVID-19 crisis.

Comments

Very interesting incentive -

Very interesting incentive - based repayment plan. However I do wonder what happens if the merchant's transaction volumes do not meet Kopo Kopo's expectations. Which leads me to a bigger point - do these merchants get the benefit of consumer protection provisions in Kenya? For example any responsible lending requirements? The concern is that often we see that such requirements only apply to credit provided for personal purposes. Arguably any credit for small business purposes should be covered as well.

Add new comment