|

In the past couple of years, merchant payments have gone from being a trending buzzword among mobile money providers and other digital financial services (DFS) players to occupying a permanent place among their top immediate priorities. Most payments providers in the more developed DFS markets have already launched a merchant payments initiative or are planning to do so in the next year. The payments providers who don’t have it on their near-term roadmap are few and far between.

It is not hard to see why. While mobile money has been extraordinarily successful in driving uptake on accounts, the business model has almost always been centered on remittances and airtime purchases, both of which are very limited markets that can deliver only so much revenue, even for successful providers. The wider retail commerce space, however, represents a vast opportunity: the World Bank has estimated that micro-, small-, and medium-sized merchants worldwide accept $19 trillion worth of cash each year; the vast majority of these merchants are in emerging markets and developing economies. In terms of numbers of transactions, the picture is even more stark: even in successful mobile money markets like Ghana, 99.9 percent of payments for consumption goods are still made in cash.

Hence the provider that succeeds in digitizing payments in the broader retail commerce space would unlock a massive and immediate opportunity: $19 trillion annually is nearly 500 times the total volume of payments made across the entire mobile money industry. (According to GSMA, the world’s 272 DFS deployments had $41 billion in transactions in 2018.)

However, the most important and valuable component of digitizing payments may be the massive amount of detailed transaction data that are generated. These data can be mined to create new products and services for the payments providers themselves and for third-party providers who have access to the data. Many DFS providers realize how important it is to collect and analyze business and customer data to inform their strategies in the medium and long terms. “China: A Digital Payments Revolution” and “The New Retail Revolution” shine a light on implications of the rapidly emerging digital merchant payments markets in East Asia.

The promise of digital merchant payments is clear, how to succeed in this space is not. Even highly successful providers in mature DFS markets often have struggled to gain traction with a merchant payments offering despite several years trying. The industry has few success stories. One reason for this is a strongly held skepticism of digital payments solutions in the retail space. (For more on this, see “Cash Is King in Merchant Payments.”)

Overcoming challenges of merchant payments in retail commerce will be difficult in most developing economies. However, providers who are receptive, reflective, and focused on the medium to long term can succeed. Business-as-usual approaches that focus on short-term revenue maximization are likely to fail.

The strengths of cash in retail commerce

Most DFS providers who are interested in merchant payments realize that cash actually works pretty well in retail commerce. Merchants and their customers find that cash has many strengths that plain digital payments solutions do not have. Providers that do not truly accept this are unlikely to succeed, regardless of the time and money they put into the service.

Moreover, being as good as cash is not good enough. Digital payments have to be significantly better for merchants and their customers in at least one respect. If not, few of them are likely to change instinctive behaviors and business processes that have been ingrained for generations. Behavioral inertia tends to be significant and overcome only with a genuinely compelling value proposition, such as the one mobile money offered over previous solutions for domestic remittances. Providers have by and large struggled to identify a similarly compelling value proposition in merchant payments. See “Merchant Payments: Adding Value for Merchants” and “Elements of a Successful Loyalty Model in Merchant Payments” for advice and insight into this challenge; see “VAS Playbook” and “Loyalty Playbook” for examples. Working capital financing is an obvious opportunity that no merchant payments provider should overlook, but there are also many others.

Providers need to keep in mind that the value of digital payments to most users lies beyond the payment itself. They find value in the features and services that can be offered on top of the payments and that address the pain points small businesses have.

Another challenge is building up enough scale on both sides of the market to get a critical mass of adoption. Here providers face a quandary: a merchant payments solution is useless to customers unless there is a very large acceptance network of merchants where they can use the solution. At the same time, merchants will not be interested in the solution until there is a wide consumer base that demands digital payments. Offering compelling value propositions and loyalty models is necessary to solve this, but it may not be sufficient. Merchant acquiring in particular is inevitably resource-intensive. Retailers will need to be convinced and on-boarded one by one.

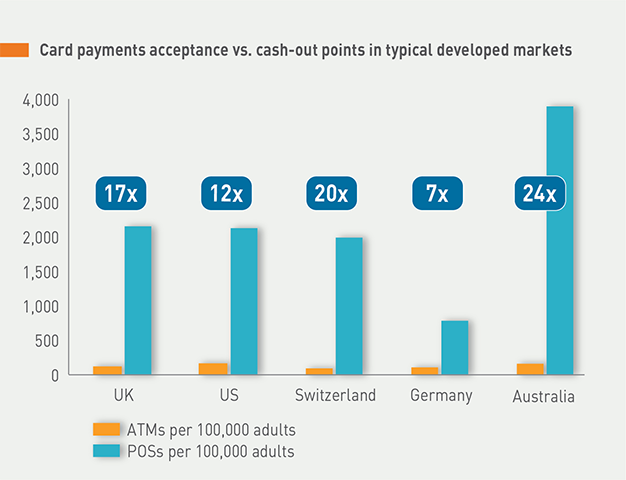

The scale of this endeavor should not be underestimated. Considering the ratio of card merchants to ATMs in developed economies, merchant networks probably have to be 10 times the size of agent networks to create true ubiquity. No single DFS provider is likely to have the appetite for making the investment required for creating such a massive distribution network all by itself. Yet that is how most providers tend to enter merchant payments: by building tailored networks of merchants that end up creating parallel walled gardens. Such turf-driven duplication results in little beyond a waste of resources and lower prospects of success for everyone involved. Instead, providers should recognize that they have more to gain by collaborating and by establishing interoperable merchant solutions from day one, as outlined in “Interoperability: Why and How Merchant Payments Providers Should Pursue It.”

Interoperability is necessary, but it may not be enough: providers should also actively encourage a vibrant market of third-party merchant acquirers. As we have seen in the card payments space in advanced economies, the development of a rich universe of third-party players in the merchant acquiring value chain can dramatically expand acceptance networks. Moreover, they can create better value for both retailers and consumers by specializing in serving specific segments with niche solutions to a degree that general payments providers never can.

Square is perhaps the most well-known example of this, having enabled card acceptance at millions of new merchants through a combination of hardware, business model, and interface innovations. But Square is just one among a vast array of players that collectively on-board and operate as many as 80 percent of card merchants in the United States. Banks largely focus on the issuing side: selling cards to consumers. Mobile money providers and other DFS players should consider how much of the merchant acquiring value chain they really want to take on. This is discussed in “Acquiring Models.”

Card payments acceptance vs cash-out points in typical developed markets

A key question for providers is the choice of acceptance technology. This is a decision of paramount importance because it has direct and major implications for the cost of building out acceptance networks and for the user experience (UX) offered to merchants and consumers. While the cost aspect is easily quantified and intensely scrutinized by chief financial officers, providers should also be careful not to underestimate UX. Slow, unintuitive, unreliable interfaces and processes will exponentially compound the weaknesses that already affect many digital payments solutions in comparison to cash. For the pros and cons of different options, see “Acceptance Technologies for Merchant Payments.”

Another challenge is how to craft a business model that drives revenue without disincentivizing uptake. Most providers tend naturally toward a reliance on transaction fees, which lie at the heart of prevailing business models for the card industry as well as for mobile money. But there is good reason to think that merchant payments initiatives founded on transaction fees will have a hard time scaling in developing economies because they directly disincentivize the very thing the business depends on—transactions—in a context where the value proposition around digital payments in retail typically isn’t very strong to begin with. This creates yet another motivation for providers to develop comprehensive offerings with value-added services that solve real pain points for users: if those services really do add value, users will be happy to pay for them.

Crucially, providers should orient their business model not around short-term priorities, but around their medium-term vision for retail commerce. This space is starting to see significant disruption as the previously separate worlds of online and offline commerce are increasingly blending together. The most ambitious business strategies for capturing value from this are on display in China, where Alibaba has identified retail as one of the five sectors of the economy primed for disruption through technology.

But signs of the same transformation are visible across developing economies, as e-commerce platforms expand rapidly while millions upon millions of informal sellers very actively use WhatsApp, Facebook, and Instagram to market their wares. This seismic shift is still in its infancy and will take time to fully play out, but it is very real and accelerating. Its broad contours are already fairly clear, as discussed in “The New Retail Revolution.” DFS providers venturing into merchant payments would be remiss not to explicitly consider this shift when developing their business models.

These considerations are linked and point in the same direction. They result in an approach to merchant payments that leverages openness to drive scale and create value through partnerships and specialization rather than the instinct to own territory and keep everything in house. They result in a business model that resists the short-term impulse for transaction fees and instead takes a broader and more patient view of the retail payments space. This model would lay the foundation for an extensive digital ecosystem and build a strategy around the use of data and the importance of being the main interface between customers and their money.

It is no coincidence that the more providers consider this approach, the more it starts to look like other visions of the medium-term strategies for DFS providers as a whole, as captured, for instance, in the recent focus by GSMA on payments-as-a-platform or by work on open APIs, platforms, and the future of banking. As the digital commerce space evolves, merchant payments will increasingly become just one piece of an increasingly seamless whole. Providers who understand this will craft today’s strategy for merchant payments in a way that plays toward the medium-term vision. The ones who do not just might not be around when the future comes to pass.