When it comes to building a revenue model for merchant payments, many DFS providers’ first instinct is to zero in on transaction fees. They focus on answering two questions: Who should I charge? And how much? But people tend to view cash payments as free of cost, making a digital payments model based on transaction fees an uphill battle. This is particularly true in developing economies, where even “small” amounts matter to people and where digital solutions are often already at a disadvantage to cash.

Providers should instead think about profitability in a longer and broader perspective as part of a suite of products and partnerships unlocked by merchant payments. This could mean using merchant payments as a loss leader to drive larger ancillary revenues. Payments data can be more valuable than transaction fees. Forward-looking providers have already realized that “data are the new oil” and are building complex suites of value-added services (VAS), bridging online and offline commerce to unlock new value pools for themselves and their customers.

Don't charge transaction fees, particularly on consumers

Budding merchant payments players in developing economies may be hard-pressed to take this advice. Yet it is something they should seriously consider because they are most likely underestimating the strengths of cash in retail commerce and overestimating the strength of their own value proposition. But it is also because transaction fees are particularly problematic from a behavioral standpoint.

The problem with transaction fees in particular is that they appear at the most sensitive time: when consumers are deciding on which payment instrument to use. Since cash is always readily available as the default option, this is the worst possible pricing model for digital payments. This is particularly true for transaction fees on end customers, who wield greater influence over the payment choice and for whom the value proposition of digital payments is already harder to build.

Fortunately, there are many alternatives to transaction fees. One is a subscription model that charges people a weekly or monthly fee in return for free transactions. This type of model has been deployed by companies like Vodafone Ghana and is a good way to generate direct revenue without the behavioral barriers created by transaction fees. Another option is to generate indirect revenue through VAS, for which there are plenty of opportunities.

Whatever the approach, providers should recognize the challenges that transaction fees create, and they should have an explicit strategy to overcome them through some combination of pricing model, pricing level and value proposition.

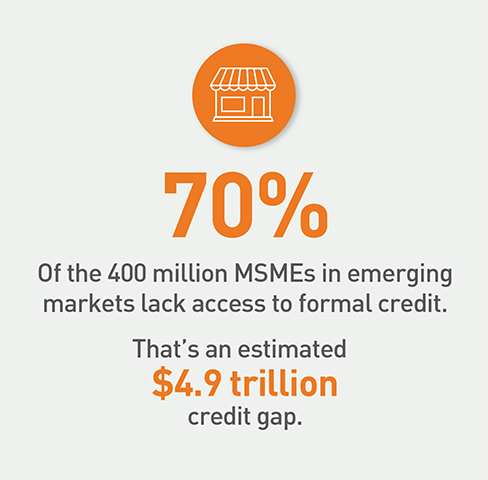

Digital credit could be the killer app for merchant payments

Small, semi-formal merchants in developing economies consistently report that one of their biggest pain points is access to capital. Digitizing merchant payments could be the key to expanding financial access while creating a strong value proposition for merchants in digital payments.

For payments providers, offering digital credit products to merchants could also be a potentially profitable opportunity, with gross margins up to 60 percent and relatively low risk due to the availability of detailed, real-time cash-flow data and the ability to deduct payments at source. If provided sustainably as part of the overall revenue model, merchant credit could be the answer to the otherwise intractable transaction fee problem. That is the reason merchant payments acquirers from Kopo Kopo to Square and PayPal have increasingly geared their businesses toward merchant credit.

The opportunity could extend to end-customers. The granular payments data from merchant payments are far more useful for scoring models than the data on telecoms use and occasional person-to-person payments that most digital credit providers rely on. Hence, digitizing merchant payments streams could help make consumer finance more accurate and responsible while providing a strong incentive for people to eschew cash for digital payments. That said, it is also subject to the same risks that CGAP has already highlighted in the rapidly expanding industry around digital consumer credit.

The advent of digital credit has extended access to instant, automated, remote credit to millions of borrowers. But who is accessing these loans? How are borrowers using the money? And to what extent are we seeing risks emerge such as late repayments and defaults, lack of

New retail is reshaping retail commerce and creating new business models

Online and offline commerce are rapidly blending into one seamless space, connected and powered by digital payments in conjunction with smart logistics systems and social media platforms to create new dynamics between consumers, producers, wholesalers, and retailers. It is furthest along in China, where Alibaba sees new retail as one of the five major transformations driven by technology, and in the United States, where Amazon is redefining the in-person shopping experience.

This shift is happening also in developing countries, but in a different way. Across the globe, many small merchants are using social media to market their wares. As they become integrated with e-commerce and delivery platforms, their businesses will start looking very different from the past, creating new economic and financial inclusion possibilities.

Digital payments sit at the heart of this transformation, enabling the seamless integration of online and offline channels while powering new types of products and services for merchants and consumers alike. Providers who position themselves for this shift will be able to create value and generate revenue in new ways. Those who do not will struggle to stay relevant as the earth shifts under their feet.

|

Continue to: Opportunity | Value Proposition | Distribution |